Myriad promises, mixed delivery

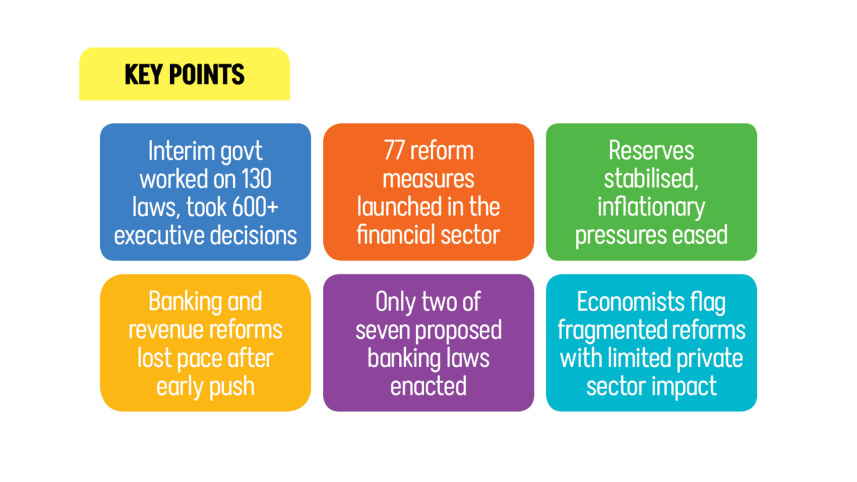

The interim government has introduced 77 reform measures across the financial sector, covering planning, finance, commerce, industry, labour, and power and energy. The initiatives helped ease some macroeconomic pressures, as falling foreign exchange reserves stabilised and inflation showed signs of moderation.

Yet, vital reforms in the banking and revenue sectors moved slowly from planning to implementation.

For instance, the Bangladesh Bank (BB) proposed amendments or new laws for seven areas, but only two -- the Bank Resolution Act and Bank Deposit Protection Ordinance -- were enacted.

Even though the Bank Resolution Act was passed in May last year, Sammilito Islami Bank, the new state-owned shariah-based lender formed through the merger of five troubled banks, has not fully started operations.

While repayments to depositors of the five banks have begun, no management team has been appointed for the merged bank.

Key proposals, such as amendments to the Bangladesh Bank Order-1972 and the Bank Company Act, critical for banking governance, have not progressed. These were not even included in the government’s new reform book, leaving their future uncertain.

Yesterday, the government published the reform book, listing achievements in public service, health and education, energy, science and IT, finance, culture, and transport.

In the financial sector, measures include revisions to insurance agent regulations and solvency margin rules for life and non-life insurers.

M Masrur Reaz, chairman and CEO of Policy Exchange Bangladesh, said the reforms undertaken so far are insufficient to support the private sector, which dominates the country’s economy.

“There was no reform strategy, so whatever reform was done is isolated and sporadic,” said the economist. “Are they of high impact for stimulating growth? No, these reforms do not have a high impact on growth and job creation.”

Reaz, however, admitted some positive initiatives, such as simplified repatriation procedures and streamlined foreign loan approvals. But he mentioned the absence of efforts to strengthen institutions like the Bangladesh Investment Development Authority (Bida).

Since taking office, the interim government has enacted nearly 130 laws, both new and amended, and taken more than 600 executive decisions, demonstrating the urgency of institutional reform, the reform book says. About 84 percent of these measures have already been implemented.

Other reforms in the financial sector include changes to microfinance banks and Krishi Bank.

In a significant move to enhance trade fairness and growth, the government introduced the Commercial Court Ordinance, 2026, establishing specialised courts with document-based trials, 90-day case disposal, mediation, virtual hearings, and online case management, according to the book.

Towfiqul Islam Khan, additional research director at the Centre for Policy Dialogue (CPD), described some reforms as “broken”.

“As the financial sector reforms were not consulted with political parties, there is doubt they will survive under a future government,” he said.

Khan also cited issues in the implementation process of public projects, which lack integrity checks and proper feasibility assessments.

He hoped the next elected government would continue reform efforts, and said that political stability depends on economic stability.

The interim government said it conducted inclusive political dialogue over seven months, culminating in the July Charter, which now awaits approval through a referendum.

The Charter aims to entrench fundamental rights, checks and balances, and safeguards against authoritarianism.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. “These reforms mark the first steps toward a reimagined system of governance -- one that serves citizens rather than dominates them,” the government said.

Asif Ibrahim, former president of the Dhaka Chamber of Commerce and Industry (DCCI), said the interim government stabilised the economy during a challenging transition. Its focus on fiscal discipline, inflation management, and financial sector oversight restored market confidence.

“Private investment momentum remained cautious, and longer-term issues related to competitiveness, productivity, and employment were only partially addressed,” he said. The administration laid a foundation of stability, leaving broader growth-oriented reforms to the next government.

Taskeen Ahmed, president of Dhaka Chamber of Commerce & Industry (DCCI), praised initiatives promoting a digital, rules-based business environment. Key measures included the BanglaBiz platform, Bangladesh Single Window for one-day licensing, Green Channel customs automation, extended bonded warehouse facilities, and the Tax Expenditure Policy.

He said legal predictability and investor confidence were strengthened by the National Strategy for Attracting FDI, specialised commercial courts, the Merchant Power Policy, and English versions of tax laws.

“Labour, ADR, and the Governance Performance Monitoring System further reduced business costs and replaced ad-hoc decision-making with transparent systems.”

But the president of Dhaka chamber criticised the government’s decision to maintain the 2026 LDC graduation timeline, ignoring calls from the business community to delay it until 2032.

Stalled structural reforms, such as the revenue board split and the lack of full autonomy for the Bangladesh Bank, continue to generate financial uncertainty, according to the business leader.

He said that effective execution is required for reforms to produce tangible results.

Ashraf Ahmed, a former president of the DCCI, highlighted several long-awaited measures, including amendments to Trade Organisation Rules, the Bank Resolution Ordinance, NBR reorganisation, and the Merchant Power Policy.

While widely welcomed, he noted that outcomes remain in flux.

“The business community is waiting to engage with NBR leadership, while depositors, shareholders, and borrowers monitor developments closely. Hopefully, future governments will carry these reforms through to unlock the benefits,” he said.

Comments