TakaPay struggles to gain traction two years after launch

TakaPay card, the first-ever national debit card, has failed to secure a significant foothold in the two years since its launch by the central bank, aimed at reducing dependency on global payment networks such as Visa and Mastercard.

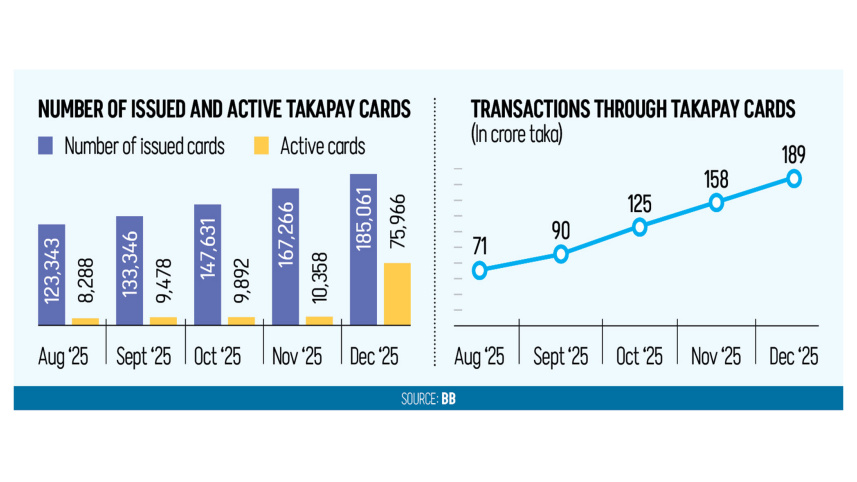

Data from the Bangladesh Bank (BB) showed a recent uptick in issuance and transactions through the TakaPay card. However, the number of cards, transactions and the amount of transactions still remain very low.

In December last year, Bangladesh recorded Tk 50,281 crore in transactions through local and foreign currency cards, the highest in six months. Of that, transactions through TakaPay were Tk 189 crore, which was less than half a percent of the total card-based transactions during the month.

Initiated by the central bank, the TakaPay card was launched in early November 2023 by the deposed prime minister, Sheikh Hasina, to save foreign currencies

The month before, transactions using the TakaPay card were Tk 157 crore, which was 0.33 percent of total transactions of Tk 47,536 crore through local and foreign currency cards.

Initiated by the central bank, the TakaPay card was launched in early November 2023 by the deposed prime minister, Sheikh Hasina, to save foreign currencies, at a time when the country was struggling to contain the fall of forex reserves. On October 31, 2023, Bangladesh’s readily usable forex reserves were below $20 billion.

The initiative also came in line with other countries that have already issued their own currency cards. For example, Sri Lanka uses ‘Lankapay’, Pakistan has ‘Pakpay’, India employs ‘RuPay’ cards, and Saudi Arabia has ‘Mada’.

Initially, three banks -- BRAC Bank, City Bank PLC and Sonali Bank PLC -- joined the foray to issue the TakaPay card, which can be used for cash withdrawals from ATMs and point of sale machines, and e-commerce transactions.

Later, 14 more banks joined. Yet, progress in the adoption of the card has been slow, mainly due to low awareness of the card among people, lack of push from banks, limited usability, and lack of benefits or incentives offered by the authorities to encourage users.

“Responses from customers have been slow. Not all banks are issuing the card,” said Md Shafquat Hossain, deputy managing director and head of retail banking at Mutual Trust Bank PLC.

MTB PLC encourages customers to opt for the TakaPay card during the opening of accounts through its agent banking outlets. “Its annual fee is lower than that of cards issued by global payment gateways,” he said.

A senior official of another private bank said the TakaPay card cannot be used for international transactions. So, customers who travel abroad or purchase from foreign markets will not take the card, he said. Besides, ATMs of all the banks are not configured to allow transactions through the TakaPay card.

“Not all the ATMs accept the card. This limits the usage of the TakaPay card,” he said. “To make the card lucrative, the authority should add some unique features to the card and motivate banks,” he said.

Md Mahiul Islam, deputy managing director and head of retail banking at BRAC Bank, said his bank is also issuing the card through its agent banking network in suburban areas.

“We are offering the card to those who do not want to do foreign transactions,” he said.

A senior official of the BB said the main rollout of the TakaPay card started in mid-2024. The progress slowed for six months after the political changeover in August of the same year. “We have been registering some progress for the last six months,” he said.

While e-commerce transactions cannot be done through the Takapay card yet, the BB wants to introduce this feature in the second half of this year, the official said.

“Once it is done, we expect a good impact,” he said. “We shall encourage banks to issue the card then.”

“As transactions through the Takapay card take place through the National Payment Switch of Bangladesh (NPSB), banks do not need to spend extra to facilitate payments,” the official said, adding that with increased usage of this card, the cost for banks will decline.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments