Budget proposes lower deposits for tax appeals

Businesses will face a lower financial burden when contesting tax demands from the next fiscal year, as the government has proposed sharply reduced deposit rates for dispute cases across different stages of appeal.

The proposed budget for fiscal year 2026-27, starting July 1, seeks to sharply cut these upfront deposits across all types of tax disputes -- income tax, VAT and customs -- at two out of three levels of the appeals process. Finance Minister Amir Khosru Mahmud Chowdhury placed the proposals before parliament on June 11.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Tax experts say the changes could make the system significantly fairer for businesses, as currently they have to deposit a large portion of the disputed tax amount, sometimes as much as 25 percent, before their case is even heard. That money sits locked up during what can be a lengthy legal process, regardless of whether the business ultimately wins.

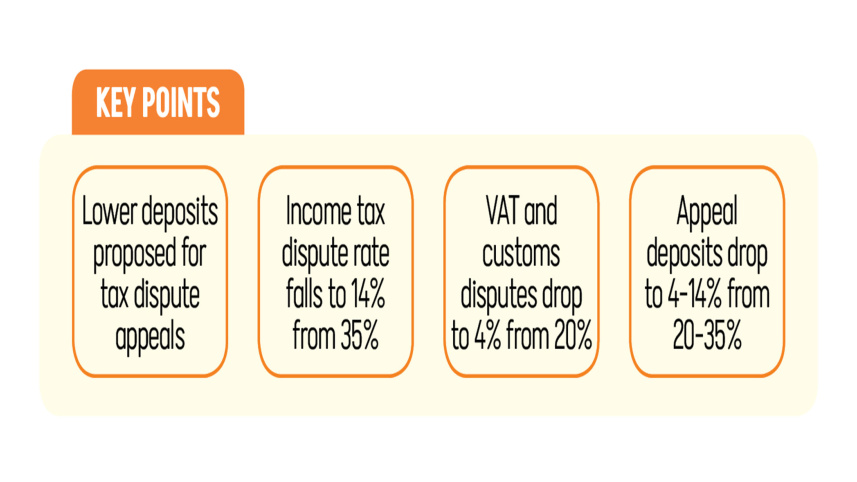

Under the proposed changes for income tax disputes, the deposit required at the First Appeal stage rises to 1 percent from zero previously. At the next stage, the Tax Appeal Tribunal, it drops to 3 percent from 10 percent. At the High Court, it falls to 10 percent from a maximum of 25 percent. The combined rate drops from 35 percent to 14 percent.

For VAT disputes, the cuts are steeper. The deposit currently stands at a flat 10 percent at all three stages. Under the proposal, it falls to 1 percent at both the First Appeal and Tribunal stages, and to 2 percent at the High Court.

If implemented, the measures will bring down the total payable rate to 4 percent from 20 percent.

For customs disputes, the rate for the first two stages drops to 1 percent from 10 percent, with the High Court rate set at 2 percent, reducing the overall rate from 20 percent to 4 percent.

The budget also proposes abolishing the power of tax officials to personally decide whether to accept or reject an appeal.

Debabrata Roy Chowdhury, company secretary and head of legal and taxation at Nestlé Bangladesh, called the move progressive.

“It would improve businesses’ access to justice and reduce the financial burden of contesting tax assessments,” he said. Previously, he noted, taxpayers had to make substantial deposits just to challenge demands, making justice costly and difficult.

He also stressed that faster disposal of cases would be essential to prevent abuse of the lower deposit requirements.

Snehasish Barua, director of financial consulting firm SMAC Advisory Services Limited, said businesses had long pushed for exactly this kind of change, noting that the previous system was largely seen as a tool for harassment.

“The prevailing complaint among businesses was that if they contested an assessor’s findings, a massive tax demand could be finalised against them. The taxpayer was then required to pay 20 percent to 35 percent of that disputed sum just to seek legal redress,” he said.

He, however, raised a concern from the other direction, noting that the deposit rate will fall to as low as 4 percent in some cases.

“Will this low threshold enable non-compliant businesses to evade immediate liability and keep disputes pending indefinitely before the High Court on a mere 4 percent deposit? Could it inadvertently institutionalise a culture of strategic litigation? These are the structural risks that policymakers and revenue authorities must tightly monitor as they execute this reform,” he said.

Speaking on condition of anonymity, another tax analyst, however, cautioned that the one percent deposit requirement at the first stage for income tax cases could also discourage some taxpayers from pursuing legitimate appeals.

An official at the National Board of Revenue said the intent behind the reform was not to make it easier to avoid paying taxes, but to make the system less punishing for businesses with legitimate grievances.

“Our preference is that revenue is collected through the regular tax system rather than through prolonged disputes and court cases,” the official said on condition of anonymity.

On the risk of misuse, the official noted that while upfront deposits have been reduced, interest charges on disputed amounts remain unchanged.

That means a business that files a frivolous appeal and loses will still owe the full amount plus accumulated interest, making delay a costly strategy in the long run.

The government also reviewed how similar systems work in neighbouring countries and other international jurisdictions before designing the proposal, the official added.

Comments