Stabilised economy, but many reforms left unfinished

When Ahsan Habib Mansur assumed office in the second week of August 2024 following a mass uprising, the financial reality was precarious.

Cheques of some banks were bouncing, many ATMs across the country were shuttered while others were awaiting routine cash supply, and the balance sheets of nearly a dozen banks were hollowed out.

Remittances and export receipts were lacklustre, commodity prices were on a wild ride, and the country had barely enough dollars to cover three months of essential imports.

By the time he left office yesterday, the financial situation had somewhat stabilised, though many economic wounds were yet to be fully healed.

During his roughly 18-month tenure as the governor of the Bangladesh Bank (BB), Ahsan H Mansur, a former International Monetary Fund (IMF) economist, was able to diagnose the economy’s ills, but he could not complete his reform agenda, according to economists and top bankers.

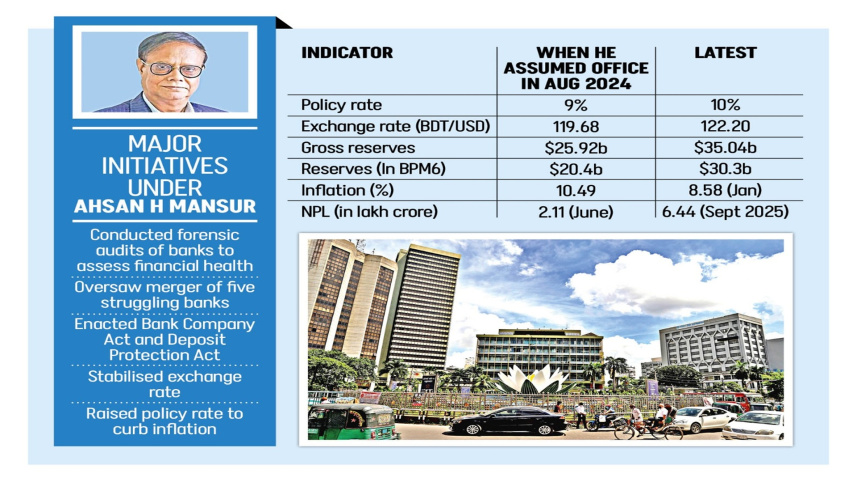

When Mansur took charge, gross reserves were $25.92 billion, and reserves as per the BPM6 count were $20 billion. Understandably, foreign exchange management was a particular area of his focus.

Mansur worked to strengthen reserves while bringing a more market-based exchange rate, a condition linked to the ongoing loan package by the IMF.

By the time he stepped down, gross reserves had risen to $35.04 billion, while the amount was $30.3 billion as per the BPM6 count. And the exchange rate has stabilised at Tk 122.20 per dollar.

Controlling inflation was another priority. It was 10.49% in the month he took office. He pursued a tight monetary policy and raised the policy rate to 10 percent swiftly after assuming office.

However, the former governor had to inject funds into ailing banks to protect depositors.

Inflation fell to 8.58 percent by January 2026, though supply-side constraints meant the decline fell short of expectations.

The banking sector presented a deeper challenge. Around a dozen of banks were sinking under heavy non-performing loans, while non-bank financial institutions were refusing to return deposits. Many bank boards were heavily influenced by politically affiliated figures.

Many bank directors reportedly fled the country with huge funds. Mansur responded with forensic audits to determine the real health of the sector and initiated reforms, though deep restructuring remained incomplete.

As long-buried toxic loans surfaced, the volume of non-performing loans (NPL) reached Tk 6.44 lakh crore in September last year from Tk 2.11 lakh crore in June 2024.

As part of his financial mess cleanup agenda, the former governor oversaw the merger of five ailing shariah-based banks, enacted the Bank Resolution Ordinance and the Deposit Insurance Ordinance. He also pushed for amendments to the Bangladesh Bank Order and the Bank Company Act, though those got stuck at the finance ministry.

While his public warnings on bank weaknesses initially spooked depositors, the measures ultimately strengthened transparency and governance.

Mustafa K. Mujeri, former director general of BIDS and ex-chief economist at the Bangladesh Bank, said, “When Mansur assumed office, it was a challenging time as the whole financial sector was on the edge of a cliff.”

“The sector had been looted. Mansur had to spend considerable time uncovering the true state of affairs,” he added.

Fahmida Khatun, executive director at local think tank Centre for Policy Dialogue (CPD), echoed similar views.

She said Mansur inherited a fragile banking sector with many banks burdened by massive non-performing loans. Bangladesh Bank had functioned largely as an implementing agency of the government, and the sector’s true health had been disguised.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. “He had to run forensic audits to review asset quality and find the real health of the banking sector,” she said.

Mustafizur Rahman, distinguished fellow at CPD, said that the outgoing BB governor made serious efforts to reform the banking sector and restore discipline during a critical period for the economy.

“His initiatives included restructuring bank boards, promoting mergers among weak institutions, setting up an asset recovery company for distressed assets and curbing illicit financial outflows, although some changes were not fully endorsed by the interim government.”

Rahman described these steps as essential not only for immediate stability but for laying the foundation for long-term governance in the sector.

Speaking on condition of anonymity, a former senior banker said Mansur demonstrated “earnest dedication and great sincerity” in his duties.

He described the former BB governor as an accomplished economist who stabilised fragile macroeconomic indicators amid post-Covid pressures, fallout of Russia-Ukraine war, and volatile global commodity prices.

“From a very dire situation, Mansur improved foreign exchange reserves and helped stabilise the taka-US dollar exchange rate,” the banker said. He added that Mansur also managed overdue petroleum and gas import liabilities and cleared remittance backlogs for airlines and shipping firms.

Comments