Bangladesh economic outlook fragile amid external shocks: PRI

Bangladesh’s macroeconomic outlook is fragile as it is increasingly facing three concurrent adverse external headwinds, including the Middle East crisis and the country’s impending graduation from the Least Developed Country category, said the Policy Research Institute (PRI) of Bangladesh today.

Uncertainty around US tariff policies is another factor that casts a shadow over the faster recovery prospects of the economy.

“These shocks are feeding through energy prices, weakened trade flows, and supply chain disruptions, with broad economy-wide implications,” said PRI Principal Economist Ashikur Rahman while presenting a keynote on Monthly Macroeconomic Insights (MMI) at the PRI office in Dhaka.

At the same time, pressure is building on the balance of payments amid weaker exports and higher energy costs, with limited policy buffers heightening overall vulnerability.

“The ongoing conflict in the Middle East is amplifying Bangladesh’s external vulnerabilities through higher energy import costs and supply chain disruptions,” he said.

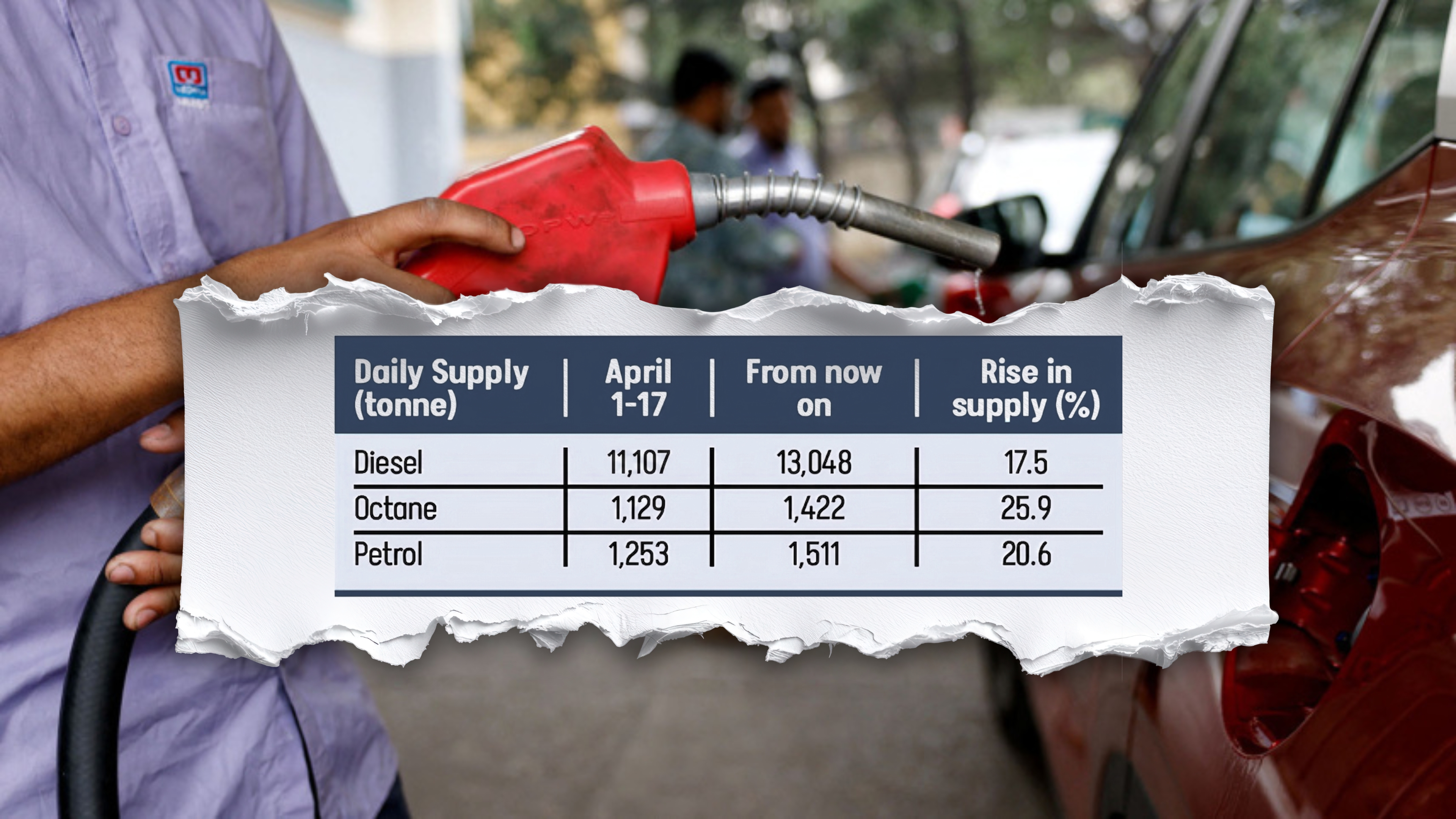

Around 31 percent of energy imports originate from the region, largely transiting the vulnerable Strait of Hormuz, exposing the economy to supply shocks, and the disruptions could raise the energy bill by 40 percent to $16–17 billion under severe price shocks in the FY26, he said, citing a study by Zero Carbon Analytics (ZCA).

PRI said Bangladesh’s economy experienced a fragile recovery over a period of 18 months up until February 2026.

Foreign reserves improved from around $18 billion in late 2024 to around $30 billion in February-March 2026, inflation moderated to 8-9 percent, and the banking sector’s deposit growth reached double digits for the last five months, indicating that some degree of confidence was being restored in the financial sector.

“Yet, this recovery was underpinned by some core vulnerabilities,” he said, citing slowing growth of the economy, which stood at 3 percent in the second quarter of FY26, the weakest since the Covid period.

The financial sector is fractured, with 30 percent non-performing loans, making banks cautious, with private sector credit growth dipping to 6 percent.

“Moreover, the fiscal space is almost absent, compelling the government to depend on high-interest-bearing short- and medium-term loans from the banking sector, and more recently, central bank financing.”

Against this backdrop, Rahman said backtracking on critical reforms in the fiscal and financial sectors only deepens existing vulnerabilities.

“At a time of heightened external uncertainty, such reversals risk amplifying rather than containing macroeconomic stress.”

He said the added uncertainty surrounding the IMF programme further sends an adverse signal to international partners and markets alike.

“This is, in many ways, a self-inflicted wound—one that the country can ill afford at this juncture.”

“What is required now is disciplined and cautious macroeconomic management grounded in fiscal and monetary prudence. Yielding to short-term populist pressures may offer temporary political comfort, but it risks undermining long-term stability.”

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments