Securing Bangladesh’s energy future

In recent weeks, energy has been one of the most discussed topics—whether in the news, seminars, articles, or the global stock market—not just for Bangladesh but for the rest of the world. Securing energy resources is key, as it determines how the economy will prosper in the years ahead.

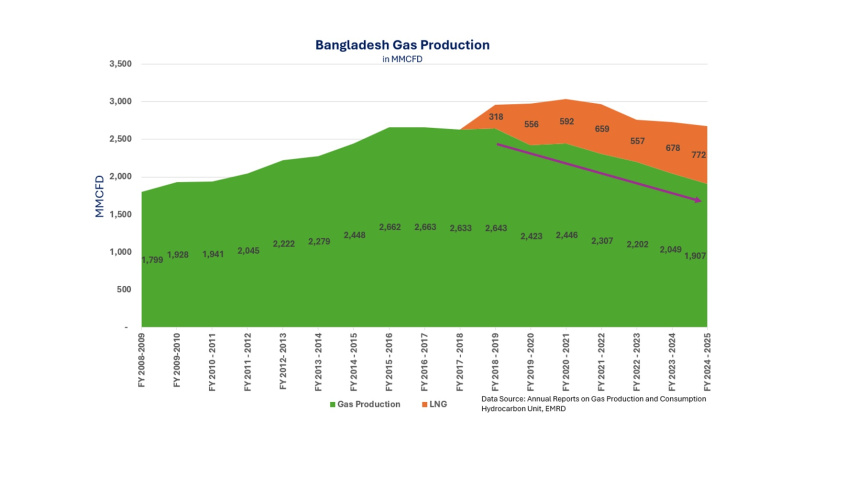

Before exploring our potential energy opportunities, I would like to briefly share our current state based on the chart above. The green area in the chart reflects Bangladesh's domestic gas production, which in recent years has included both national companies—Bangladesh Gas Fields Company Limited (BGFCL), Sylhet Gas Fields Limited (SGFL), Bangladesh Petroleum Exploration & Production Company Limited (BAPEX)—and international oil companies such as Chevron.

In the last six fiscal years, gas production has declined by about 30 percent. This sharp decline has led to increased dependence on liquefied natural gas (LNG) imports. Based on Petrobangla’s daily production report (available on the Energy and Mineral Resources Division site), the trend continues in 2026, with domestic gas production in the range of 1,700–1,750 mmcfd.

According to the Hydrocarbon Unit, Energy and Mineral Resources Division (EMRD) annual report (2024–2025), major sector gas consumption was as follows: power (41 percent), industry (19 percent), captive (17 percent), domestic (11 percent), fertilizer (6 percent), and the remainder by CNG and commercial.

Steps to strengthen energy security

Onshore:

It will be important to develop a comprehensive asset plan and carry it through to reach the full potential of each gas field. Some fields may require workovers, debottlenecking, new compressor projects, or better management of production losses through predictive maintenance.

Robust planning and the use of technology can also improve the efficiency of turnarounds—for example, by using robots for tank inspections, drones for flare inspections, and reducing the number and duration of shutdowns. In the oil and gas industry, we often say that every barrel matters.

In addition, each asset should carry out an exercise to identify any additional resources that could potentially be converted into reserves and ultimately into production, without applying constraints such as gas pricing, costs, budget limits, or other resourcing challenges. Running an unconstrained exercise like this helps shift the mindset from “what cannot be done” to “what we can do.”

The opportunities identified through this process, even those not currently economically viable under existing terms or blocked by other constraints, should be prioritized and escalated for discussion so that those barriers can be addressed quickly.

LNG spot prices are currently several times higher than domestic gas. Given this gap, onshore opportunities should be accelerated with urgency as part of our broader energy security strategy.

Offshore:

We will need to entice IOCs with the right fiscal incentives; otherwise, every bid round will fall behind in terms of timeline. Several technological advancements have taken place in recent years, including modern OBN (ocean bottom node) seismic, the use of AI for faster prospect maturation and better imaging, the first high‑pressure (20K PSI) wells drilled in the anchor project, future cost‑effective tieback opportunities when discoveries are too small for standalone facilities, and advanced remote operations. Offshore projects remain some of the longest and most complex in the oil and gas portfolio.

LNG:

It is important to understand how the LNG trade flow is shaping up now. The majority of the world’s LNG demand is in Asia. In other regions, Europe used to be dependent on Russia. Since the Russia-Ukraine war, Europe has rapidly shifted and started relying on LNG from the U.S. According to the American Petroleum Institute (API), Europe has become the largest destination for U.S. LNG, with a record 67 percent going to the EU and UK between January and April 2025. This trend is most likely to continue in the near future.

Reuters reported that about 90 percent of Australia’s LNG exports go to Japan, South Korea, and China. LNG expansion from the African region will likely target Europe and other Asian countries.

According to the IEA, Bangladesh, India, and Pakistan imported almost two-thirds of their total LNG supplies through the Strait of Hormuz in 2025. As our contracted LNG is now impacted, we are increasingly dependent on the spot market.

According to various newspaper reports, it is encouraging to see that Bangladesh is managing to secure several LNG cargoes for April. Going forward, as Bangladesh continues to compete for LNG with other Asian countries, it would be a good strategy to limit our exposure to spot prices. Along with Qatar, which will likely remain a longer-term, affordable supplier, we must secure backup options by arranging term contracts from non-Middle Eastern countries.

A Hybrid Approach

To ensure Bangladesh's energy security, we will need a hybrid approach that includes:

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. - Extending the onshore production plateau through both national companies and IOCs.

- Addressing power needs by providing incentives for solar and accelerating other renewable energy.

- Expanding storage capacity for crude oil and refined products.

- Attracting IOCs to explore offshore blocks.

- Balancing gas demand and supply through longer-term LNG contracts sourced from different regions.

Shahid Shamsu is an oil and gas professional with more than 20 years of experience. Views expressed in this article are the author’s own. He can be reached at: sshamsu@alumni.harvard.edu

Comments