Next 180 days will be challenging for the newly elected government

A roundtable titled “Looking into Bangladesh’s Development: Priorities for the Newly Elected Government in the Short to Medium Term” was held on March 4, 2026, at the BRAC Center, Dhaka. The event was jointly organised by The Daily Star and the Centre for Policy Dialogue (CPD). The discussion convened policymakers, economists, representatives from both public and private economic and financial sectors, and development practitioners to reflect on Bangladesh’s current economic challenges and outline key priorities for the new government. Against a backdrop of high inflation, fiscal constraints, and slowing investment, participants emphasised the urgency of restoring macroeconomic stability, strengthening governance, and accelerating reforms. The roundtable also highlighted the significance of Bangladesh’s upcoming LDC graduation and the need for a strategic, well-coordinated transition to sustain growth and competitiveness.

Dr Fahmida Khatun

Executive Director

Centre for Policy Dialogue (CPD)

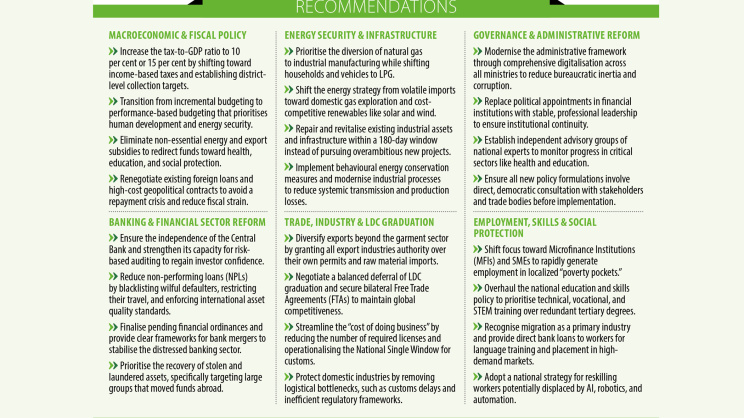

The current macroeconomic landscape of Bangladesh is navigating a period of multifaceted pressure, characterised by high inflation, a narrowing fiscal space, and a vulnerable banking sector. While real GDP growth showed a downward trend starting in 2022, a slight recovery emerged in early 2026, suggesting a gradual pickup in economic activity. However, headline and food inflation remain significant concerns, as stagnant wage growth continues to erode the public’s purchasing power. The investment climate remains sluggish; private sector credit growth has hit a decade low, while the government’s reliance on banking sector loans has surged to fill fiscal gaps. To restore stability, the focus must shift toward synchronising monetary and fiscal policies while addressing supply-side bottlenecks in the food market. Enhancing fiscal discipline is critical, as the tax-to-GDP ratio remains one of the lowest in the region, and the national debt is rising. In the banking sector, reducing non-performing loans, which spiked due to recent asset quality reviews, and ensuring the independence of the Central Bank are non-negotiable for regaining investor confidence. Furthermore, as the nation approaches LDC graduation, diversifying exports beyond the garment sector and streamlining customs and logistics will be essential to maintaining global competitiveness and protecting foreign exchange reserves.

Mahfuz Anam

Editor and Publisher

The Daily Star

Effective governance relies less on policy design and more on the efficiency of implementation, which is currently hindered by a bureaucratic system characterised by colonial-era obstructions. Over-regulation often leads to significant project delays, causing costs to escalate far beyond original budgets and placing an unnecessary burden on public funds. To address this, the government must modernise the administrative framework through comprehensive digitalisation. Moving beyond financial systems to include all ministries will enhance efficiency and drastically reduce systemic barriers. Furthermore, establishing independent advisory groups for critical sectors like health and education would allow the government to leverage national expertise. These groups could provide quarterly insights and monitor progress, ensuring intellectual capital informs state functions. Success in this volatile global climate requires moving past bureaucratic inertia toward a collaborative, expert-driven model that views the nation’s economic stability as a collective challenge for both the government and the people.

Dr Rashed Al Mahmud Titumir

Hon’ble Prime Minister’s Adviser

Ministry of Finance & Planning

Prime Minister’s Office

Addressing the current economic crisis requires a shift from a consumption-led growth model to one driven by sustainable investment, supported by a mandate for comprehensive state reform and the restoration of a fragile economy. Strategic priorities include moving toward “universal social protection” through a digital public infrastructure, specifically a “One Citizen, One Card” system, to eliminate fiscal leakages and ensure aid reaches the truly vulnerable. Immediate fiscal actions have already begun, such as waiving interest for 1.2 million farmers and supporting the garment sector to ensure stability without industrial unrest. The long-term vision focuses on enhancing domestic capacity and “strategic pragmatism” in revenue management. This involves transitioning from arbitrary tax exemptions to performance-based incentives and aiming to raise the tax-to-GDP ratio to 15 per cent by 2035. To tackle the unsustainable 60,000 crore BDT energy subsidy, the administration is pursuing a three-pronged strategy: renegotiating expensive contracts based on geopolitical and domestic interests, reducing systemic transmission losses, and boosting local production. Furthermore, activating the capital market is essential to move away from a debt-ridden model; currently, low market capitalisation and structural non-performing loans (NPLs) necessitate a deeper bond market and the prevention of insider trading to foster public ownership in the economy. Regarding LDC graduation, the stance is to seek a balanced deferral from the UN, ensuring that the transition only occurs once the country achieves necessary competitive productivity and export diversification.

Dr Sadiq Ahmed

Vice Chairman

Policy Research Institute (PRI) of Bangladesh

Bangladesh faces a precarious economic landscape marked by plummeting GDP growth, rising poverty, and high inflation. To reverse this, reforms must prioritise fiscal sustainability, balance of payments (BOP) stability, and restoring the banking sector’s health. Currently, the government is unsustainably borrowing from banks to cover current expenses. Fiscal recovery requires raising the tax-to-GDP ratio from 6.5 per cent to 10 per cent by shifting toward income-based taxes and transforming state-owned enterprises into profit-yielding assets. Furthermore, eliminating non-essential energy and export subsidies could save nearly 2 per cent of GDP, allowing for doubled spending on health, education, and social protection. Finally, with non-performing loans reaching 36 per cent, the banking sector faces a serious risk of instability. To prevent further decline, two urgent steps are needed. Banks that do not meet Basel III standards should be restricted from issuing new loans and operate in a limited capacity. At the same time, all banks must focus on recovering existing loans. Lending should only resume once they meet the required standards through recovery efforts and fresh capital injection.

Dr Mohammed Helal Uddin

Executive Vice Chairman

Microcredit Regulatory Authority

Current banking data reveals a severe systemic crisis, with 26 banks reporting negative deposit growth and most struggling to maintain liquidity. This internal weakness makes the formal banking sector an ineffective channel for rapid job creation. To generate employment rapidly, the focus must shift to the informal sector and Microfinance Institutions (MFIs). These institutions currently manage significant loan portfolios with high recovery rates and possess the localised capacity to reach “poverty pockets” that traditional banks cannot. Providing aggressive financial support through MFIs for youth and self-employment initiatives is a more viable path to reducing inequality. Furthermore, while inflation remains high, it is increasingly driven by supply-side issues rather than excess demand. So, continuing to suppress demand through high interest rates is likely ineffective and risks deeper economic contraction. The government should transition its focus toward supply-side interventions to support essential commodities for targeted low-income groups. Stabilising inflation at its current level while shifting the gear toward production and employment is essential to prevent a broader social and economic crisis.

A K Azad

Vice President

International Chambers of Commerce Bangladesh (ICC)

The current economic situation requires a shift in focus from government spending to supporting the private sector and industrial growth. High rates of unpaid bank loans, particularly in state-owned banks, are a major hurdle; while legitimate businesses need support, the government must take a firm stand against those who take money without investing it. To fix the declining growth and revenue, the primary focus must be on energy security. Instead of using natural gas for household stoves or cars, it should be diverted to factories to keep machines running and people employed. Households and vehicles can switch to LPG, allowing the industry to flourish. Additionally, the cost of doing business is too high compared to neighbouring countries that offer better subsidies and cheaper utility rates. The government should trim down bloated bureaucracies and cut unnecessary expenses, such as excessive security details for officials. By reducing wasteful spending and ensuring that gas and electricity reach the manufacturing sector, the country can create more jobs, increase tax revenue, and naturally stabilise the economy.

Doulot Akter Mala

President

Economic Reporters Forum (ERF)

Despite changes in government, deep-rooted issues in the financial sector often persist due to a stagnant bureaucratic mindset. Currently, the revenue sector is struggling with a tax collection shortfall of approximately 60 billion BDT, even as targets are being raised. A major concern is the lack of transparency; the government must publicly identify wilful loan defaulters and tax evaders to send a strong message of accountability. Furthermore, the frequent resignation of heads of financial institutions during regime shifts creates instability, suggesting a need to move away from political appointments toward a more professional, stable leadership. To fix the economy, policy-making must involve direct consultation with stakeholders and the media to avoid “surprise” tax hikes that eventually fail. While the previous interim government initiated numerous ordinances and commissions, the priority now is sorting and implementing the most effective ones, such as recovering stolen assets. Internal loopholes and corruption, often protected by vested interests, must be addressed before blaming external global crises to hide our own failures.

Showkat Aziz Russell

President

Bangladesh Textile Mills Association (BTMA)

LDC graduation presents a paradox where theoretical benefits like enhanced national branding, better credit ratings, and increased foreign investment are being contradicted by reality, as evidenced by a struggling banking sector and a five-year low in foreign direct investment. While graduation will inevitably terminate access to soft loans and NGO grants, the domestic industrial environment remains stifled by complex land disputes and infrastructure delays. Instead of pursuing overambitious new projects, the government should prioritise repairing existing assets within the next 180 days. Specifically, hundreds of closed garment and textile factories representing massive investments often collapse due to minor liquidity gaps or banking failures, such as the inability to open back-to-back LCs. Moving beyond superficial debt rescheduling to provide genuine refinancing and timely financing is critical. Revitalising these existing industries is a more viable path toward economic stability than seeking new industrialisation in a time of restricted electricity, gas, and capital.

Dr M. Masrur Reaz

Chairman

Policy Exchange Bangladesh

The new administration has inherited a fragile economy where fiscal discipline has effectively collapsed since 2015-16, characterised by declining revenue, high debt, and low-return spending. A tiny fraction of the population pays taxes, while massive tax exemptions further limit the government’s ability to spend. Borrowing has surged, and the cost of repaying these loans is reaching a critical level where it consumes nearly all available revenue. To regain control, the government must move away from “incremental budgeting”, simply increasing last year’s figures, and adopt “performance-based budgeting” that prioritises human development and energy security over low-impact infrastructure. Strategic renegotiation of existing loans is essential to avoid a repayment crisis. Furthermore, the state should leverage its vast assets to raise equity rather than relying solely on bank loans. Ultimately, fixing internal project management and creating a predictable investment climate are more vital for stability than chasing ambitious growth targets through further debt.

Dr M Asaduzzaman

Former Research Director

Bangladesh Institute of Development Studies (BIDS)

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The current geopolitical instability in the Middle East poses a severe threat to energy security, particularly for a nation heavily reliant on imported primary fuels. Addressing this requires balancing energy supply with demand-side management across households and industries. While high uncertainty and rising costs of LNG threaten food security and nutrition, the long-term solution lies in transitioning to renewables like solar and wind, which are becoming increasingly cost-competitive and scalable. Future investment decisions must be cautious, as poor choices in fossil fuel infrastructure can lead to decades of financial strain through capacity payments and exorbitant foreign supplier contracts. On the demand side, substantial savings can be achieved through behavioural changes, efficient lighting, and circularity in industrial processes, especially in textiles and construction, where recycling remains underdeveloped compared to global standards. Furthermore, popularizing solar pumps and water-saving techniques in agriculture can significantly lower energy consumption during dry periods, ensuring a more resilient and efficient energy future.

Mohammed Nurul Amin

Former Chairman

Association of Bankers, Bangladesh Limited (ABB)

Restoring banking sector functionality and depositor trust is an urgent priority, particularly for distressed banks facing declining deposits and negative asset growth. Mergers alone will not resolve the crisis if underlying inefficiencies persist and banks rely on central bank financing to meet costs. Immediate steps are needed to finalise pending financial ordinances and clarify the merger framework to ensure market stability. Private sector credit growth remains weak at 9 per cent, constrained further by government borrowing that crowds out liquidity. Strengthening coordination between fiscal and monetary policies, including better alignment of interest rates, is essential. Developing the capital market, currently only 12 per cent of GDP, is critical for long-term financing. Enhanced risk-based supervision by the central bank and stronger efforts to recover laundered assets must also be prioritised.

Dr Mostafa Abid Khan

Trade specialist and former Member of

Bangladesh Tariff and Trade Commission

Success in a shifting global market requires moving away from the “business as usual” mindset and the cycle of dependency on government or foreign aid. With major competitors like India gaining duty-free access to key markets by 2027, the focus must shift toward radical policy and behavioural changes. A critical priority is reforming the education system to prioritise technical and vocational skills over redundant tertiary degrees, as the current mismatch stifles industrial productivity. To improve efficiency within the next 180 days, the government must fully operationalise the National Single Window (NSW) and adopt a risk-management approach to customs to reduce release times from weeks to hours. Furthermore, implementing the National Tariff Policy is essential to phase out long-term protectionism, forcing industries to become globally competitive. Transitioning the government’s role from “controller” to “facilitator” by simplifying micro-level licensing and activating industrial parks like the CETP and API is vital for sustainable growth.

Asif Ibrahim

Former Director, BGMEA

Vice-Chairman, NewAge Group of Industries

Rising unemployment and declining female labour force participation call for urgent reforms in investment and labour policies. While foreign direct investment has weakened, local entrepreneurship can drive job creation if bureaucratic barriers are reduced, particularly by streamlining the BIDA Act and eliminating overlapping approvals. Targeted incentives remain necessary to encourage private investment in high-growth sectors such as manufacturing, IT, and renewable energy. The SME Policy 2019 should be updated to simplify licensing and expand access to low-interest credit. The National Skills Development Policy 2011 also requires an industry-led overhaul to better align skills with market demand. Finally, updating environmental and labour regulations is essential to support green investment and increase female workforce participation.

Dr Md. Main Uddin

Professor

Department of Banking and Insurance, University of Dhaka

The restoration of banking discipline requires immediate accountability for high-profile figures, including lawmakers and regulators, ensuring they settle their personal loan instalments transparently. Addressing non-performing loans (NPLs) through temporary rescheduling or low down payments has failed repeatedly; instead, Bangladesh should adopt stringent measures like China or Malaysia by publicly blacklisting wilful defaulters and restricting their travel. Furthermore, asset quality reviews (AQR) must be standardised using international firms across all banks to ensure consistency. To activate the capital market, single-borrower exposure should be capped at 10 per cent of a bank’s capital, forcing large corporations to seek diverse funding. Ultimately, reducing NPLs from their current crisis levels to international standards depends on unwavering political will to punish defaulters without exception, regardless of their status or influence.

Amrita Islam

Deputy Managing Director

Picard Bangladesh Ltd

Addressing the “jobless growth” phenomenon is critical right now for a nation of 178 million, especially as tertiary unemployment has surged to 13.5 per cent. Export diversification, particularly in the footwear and leather goods sector, offers “low-hanging fruit” to mitigate economic vulnerability, yet progress is stalled by glaring policy discrepancies. Unlike the garment industry, other export sectors lack the authority to issue their own utilisation and export permits, forcing a reliance on bureaucratic hurdles at the NBR. Furthermore, while competitors like Vietnam require only eight licenses to start a factory, Bangladesh remains uncompetitive with twenty-three. To capture the investment shifting away from high-capacity neighbours like Cambodia, the government must prioritise technology transfer and FDI. Transforming the demographic dividend into a genuine asset requires a “jobs-first” approach that moves beyond rhetoric to implement specific logistical and regulatory reforms, ensuring that the cost and speed of doing business no longer hold back industrial expansion.

A K M Fahim Mashroor

Chief Executive Officer

Bdjobs.com Limited

Migration must be recognised as the nation’s largest industry, contributing 15 per cent to the national income and providing double the net foreign reserves of the garment sector. Despite being the economy’s lifeline, the banking sector has failed to invest in this industry, even though it offers a high return on investment with a short payback period of eighteen months. Given domestic constraints like energy shortages that hinder large-scale manufacturing job creation, the most viable “low-hanging fruit” for employment is sending 3 to 4 million people abroad within the next three years. This strategy should shift focus from the Middle East to high-demand markets like Japan, China, and Europe. To succeed, banks must provide direct loans to students and workers for language training and education abroad. Sending younger individuals for technical training in these developed markets will ensure a sustainable flow of remittances and long-term economic stability.

Mirza Nurul Ghani Shovon

President

National Association of Small & Cottage Industries of Bangladesh (NASCIB)

To drive widespread employment, the government must prioritise industrialisation at the grassroots, district, and village levels. Essential institutions such as the SME Foundation, BSCIC, and the National Skills Development Authority (NSDA) currently lack the necessary strength and require significant reinforcement to be effective. Reintroducing district-specific credit programmes, modelled after successful 1990s initiatives, is vital to provide small entrepreneurs with accessible financing. Furthermore, nearly 3,000 registered Skills Training Providers (STP) centres should be utilised for long-term skills development, while loan interest rates for small businesses must be brought down to single digits. Addressing non-performing loans requires a national or regional verification committee involving diverse stakeholders, rather than just bankers, to distinguish between wilful defaulters and those failing due to systemic issues. Ultimately, creating millions of jobs depends on a unified national political commitment where both the government and opposition align on a shared economic vision for the country’s development.

Syed Almas Kabir

Chairman, Bangladesh ICT & Innovation Network (BIIN)

Former President, BASIS

Bangladesh’s long-standing economic reliance on cheap labour, particularly in the RMG and freelance sectors, must transition toward a high-skill, value-added model to survive the challenges of LDC graduation and automation. Implementing a national strategy for reskilling workers displaced by AI and robotics is critical, alongside fostering indigenous Intellectual Property (IP) through incentivised R&D and industry-academia collaboration. The IT sector offers an ideal path for diversification due to its low overhead and potential for female empowerment, yet it requires robust soft and hard infrastructure. Effective digitalisation across government agencies, especially the NBR, hinges on structured change management and dedicated budgets for software rather than just hardware. Furthermore, prioritising local value addition in state projects and refining FDI policies to ensure knowledge transfer is essential. Strengthening the startup ecosystem through improved Venture Capital policies and expanding digital market access for SMEs will further solidify the economic backbone, while exploring innovative green energy like wave power can ensure sustainable growth.

Mahmud Hasan Khan (Babu)

President

Bangladesh Garment Manufacturers and Exporters Association (BGMEA)

The current government’s initial focus on deregulation and accessibility offers a positive trajectory for addressing long-standing systemic hurdles. A primary concern involves the formulation of policies without adequate stakeholder engagement, often exacerbated by a rigid bureaucratic mindset. To foster a sustainable industrial environment, policies must remain consistent, preventing the common issue where sudden regulatory shifts undermine new investments. Enhancing the “ease of doing business” is directly linked to reducing the “cost of doing business,” particularly regarding NBR-related complexities. Furthermore, expanding benefits like Free of Cost (FOC) raw material imports to all export sectors, not just garments, is essential for true export diversification and foreign reserve growth. To improve the tax-to-GDP ratio, implementing district-level tax collection targets could bring wealthy individuals outside major cities into the tax net, provided local trade bodies are democratically elected to avoid regional oligarchies. Finally, the decision to seek LDC graduation deferment is a strategic necessity, providing a critical window to negotiate essential bilateral agreements to ensure long-term economic resilience.

Shams Mahmud

Former President, DCCI

Honorary Consul, Federal Democratic Republic of Ethiopia

The immediate priority for the government must be renegotiating GSP terms, as the reduction in export thresholds and the 6 per cent single-country origin cap pose significant threats to the garments sector after LDC graduation. To mitigate these detriments, the focus should shift toward securing Free Trade Agreements (FTAs) and deeper regional supply chain integration with ASEAN and India. Furthermore, a government-managed long-term fund is necessary to facilitate double-stage transformation, bypassing the collateral bottlenecks of private banking. Structural reforms in energy security, logistics, specifically removing navy-led chemical testing delays, and establishing direct shipping routes are critical for maintaining efficiency. Finally, the investment climate requires a shift from a “poverty-alleviation” mindset to an investment-seeking one, prioritising joint ventures over standalone FDI, reforming the tax incidence on AIT, and stabilising the volatile stock market to build investor confidence.

Shafiqul Alam

Lead Energy Analyst

Institute for Energy Economics and Financial Analysis (IEEFA)

The current energy crisis in Bangladesh is primarily a result of an import-dependent strategy that now sees 62 per cent of primary fuel sourced from volatile global markets. With crude oil and spot LNG prices climbing, the government faces a severe fiscal bottleneck, making supply rationing and load-shedding an inevitable short-term outcome. To navigate this, the immediate priority must be clearing the massive payment backlog to sustain industrial activity while embedding energy conservation into national behaviour to prevent “rebound effects.” While IMF pressure to adjust tariffs persists, further price hikes risk making local industries non-competitive against regional rivals like Vietnam. Instead of just raising prices, the focus should shift to systemic efficiency and reallocating it to the productive sector. Long-term stability requires shifting toward regional hydropower cooperation and setting realistic renewable targets, supported by a significant shift in budgetary allocation toward domestic gas exploration rather than just power generation.

Comments