A relentless burden of debt servicing

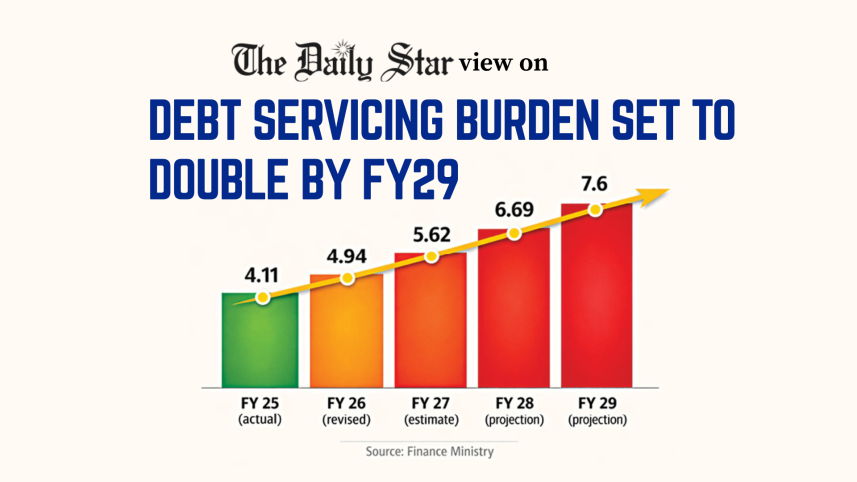

When it comes to paying back loans, timing is everything. The BNP government has come to power during one of the most challenging times for Bangladesh, considering our external debt. The government has inherited a debt servicing burden of about $4.94 billion in 2026, which has been projected to almost double to $7.6 billion by 2027. Debt repayments are made mainly in the US dollar, which has become increasingly stronger, making credit bills all the more expensive. Tackling this burden will require a combination of fiscal, monetary, export, and debt management measures.

The formidable level of external debt is attributed to rising interest payments, shorter loan maturities, and repayments for several mega projects, all of which weigh on public finances. After announcing a mammoth budget of Tk 9,38,000 crore, the finance minister has said that the government is determined to shift Bangladesh from a debt-driven economy to an investment-led one, which is essential for sustainable growth. He has talked about overhauling the public financial architecture to fund the budget and minimise the debt burden on the economy. At a Centre for Policy Dialogue (CPD) event, he stated that the country should not keep looking towards the World Bank, International Monetary Fund (IMF), and Asian Development Bank (ADB) and instead restructure our own public financing.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

While these words are meant to reassure, the sheer amount of foreign debt burden, accumulated over the years and now due for payment, cannot help but be a cause for worry. How are we going to pay off the existing dues?

Fiscal analysts believe that both expenditure composition and revenue mobilisation must go hand in hand. Which means increasing the revenue-to-GDP ratio is essential. Bangladesh’s tax-to-GDP ratio, among the lowest in the world, must be improved. The current government is considered to be business-friendly, but this should not deter it from improving income tax collection from higher earners, especially corporations.

External borrowing must be far more cautious and conservative than in the past. During the AL regime, jumping into innumerable exorbitant mega projects without proper assessments led to this punishing debt burden. The Karnaphuli Tunnel, for instance, which cost Tk 10,689.42 crore, is considered one such project built without a proper feasibility study. This has led to huge losses and an interest payment on the $705 million loan taken from China for the tunnel. The government must therefore take lessons from the AL government’s blunders and ensure that all future borrowing focuses on projects with strong economic returns. Policies must rebuild foreign exchange reserves and encourage remittances through formal channels. Besides, a credible monetary policy must be in place. Export diversification must be prioritised by expanding sectors other than ready-made garments—such as pharmaceuticals, leather, and IT services.

The government must also attract foreign direct investment to reduce dependence on external debt by simplifying regulations, improving energy reliability, and developing special economic zones. Above all, the government’s ability to manage external debt efficiently will largely depend on its political will to drastically clamp down on corruption in all its ministries and institutions, borrow strategically, spend wisely and tax fairly.

Comments