Bangladesh must decide: Compete for global capital or settle for less

Bangladesh stands at a decisive crossroads. A newly elected government has taken office. Expectations are high. Markets are watching. Investors, both domestic and foreign, are recalibrating their outlook.

The question is simple: will Bangladesh position itself as a serious competitor for global capital, or allow uncertainty to constrain its economic ambition?

For decades, global companies have helped build critical pillars of Bangladesh’s economy. Unilever Bangladesh has manufactured locally for decades, building supply chains that empower thousands of entrepreneurs. Standard Chartered Bank Bangladesh has facilitated cross-border trade and capital flows for more than a century. MetLife contributes 80 percent of the total income tax paid by the insurance industry to the national exchequer. In the country’s digital backbone, Grameenphone, alongside Robi and Banglalink, has invested billions of dollars to connect Bangladesh to the global digital economy.

These are not speculative investors. They are long-term partners.

Yet annual foreign direct investment remains below 1 percent of GDP, far behind peer economies such as Vietnam. The difference is not demographics. It is not market size. It is confidence. Perceived risk has accumulated over time.

Foreign investors bring long-term capital, advanced technology, knowledge transfer and global governance standards. They strengthen the energy, telecoms, banking, manufacturing and export sectors. Notably, just 198 members of the Foreign Investors’ Chamber of Commerce and Industry (FICCI) contribute nearly one-third of national revenue collection, an extraordinary concentration that underscores both their importance and the need for long-term sustainability.

Large-scale investment decisions are not emotional; they are mathematical. From the perspective of existing investors who have built substantial operations over decades, believed in the country and risked their capital, the evaluation centres on predictability, regulatory stability, capital mobility, tax symmetry and the efficiency of dispute resolution.

POLICY PREDICTABILITY MUST BE NON-NEGOTIABLE

Large-scale infrastructure investment requires long-term clarity and policy predictability. When policy direction shifts frequently or short-term fiscal objectives override long-term sector planning, investment confidence weakens.

Over the years, parts of the telecoms sector have been approached through a short-term revenue-maximisation lens rather than a long-term infrastructure strategy. Despite global technological convergence, Bangladesh has maintained a fragmented licensing framework, introducing multiple intermediary layers such as ICX, IIG, NTTN, TowerCo and other infrastructure categories. While each was introduced with specific policy objectives, the cumulative effect has restricted efficiency gains from experienced operators, increased structural complexity and raised service delivery costs, ultimately affecting consumers.

Predictability does not mean rigidity. Regulation must evolve with markets. But it should evolve through transparent consultation, consistent application and a forward-looking strategy.

For global investors, the central question is straightforward: can long-term capital be deployed with confidence that rules will remain stable, proportionate and consistently applied?

Institutionalising consultative policymaking, ensuring regulatory neutrality, aligning competition measures with global best practice, and anchoring sector strategy in long-term digital objectives would send a powerful signal.

Predictability is the strongest lever to unlock new capital from both existing and prospective investors.

RATIONALISE SECTOR-SPECIFIC TAXATION

Bangladesh’s telecoms, banking, insurance and financial sectors face disproportionately high tax burdens compared with regional benchmarks.

The telecoms sector carries one of the highest effective tax burdens in the region. While revenue mobilisation is important, excessive sector-specific taxation reduces reinvestment capacity and slows digital infrastructure expansion.

A sustainable economy must balance tax rates with a broad tax base. When the tax net remains narrow, governments often rely on sector-specific taxation, a practice uncommon in mature economies. In Bangladesh, this imbalance has disproportionately affected telecoms, banking, insurance and financial services.

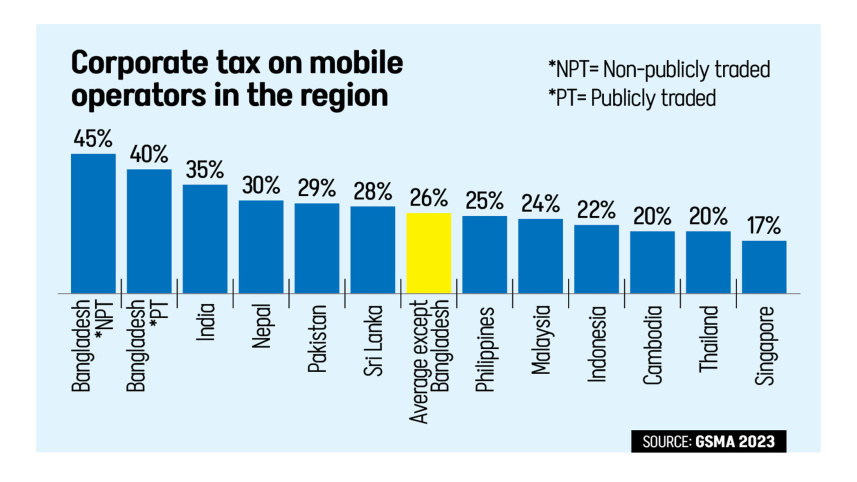

While the general corporate tax rate can be as low as 20 percent, mobile network operators face 40 percent for listed companies and 45 percent for non-listed ones, significantly higher than the regional average of around 26 percent. Banking, insurance and financial institutions also face elevated corporate tax rates ranging from 37.5 percent to 40 percent. Such high sector-specific taxation limits reinvestment and discourages foreign direct investment at a time when Bangladesh needs fresh capital to accelerate growth.

Telecoms consumers pay an effective 39 percent indirect tax on services, alongside SIM taxes and other levies. Operators additionally bear import duties, spectrum fees and mandatory revenue sharing.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. In 2025, Grameenphone’s contribution to the national exchequer was approximately equivalent to 77 percent of its reported revenue.

While rationalising sector-specific taxes may raise short-term revenue concerns, a more balanced framework would stimulate investment, expand the tax base and generate stronger, more sustainable government revenues over time.

Strategic recalibration is needed, including a gradual reduction of supplementary duties and sector levies, alignment of taxation with regional benchmarks, and incentives for growth sectors.

The goal should be long-term revenue sustainability driven by growth, not short-term extraction.

ENSURE A LEVEL PLAYING FIELD IN THE DIGITAL ECONOMY

The digital ecosystem has evolved. Telecoms operators invest billions in networks under strict regulatory and fiscal frameworks, while global digital platforms operate under different compliance structures.

This asymmetry creates a structural imbalance.

Mobile network operators and fixed broadband internet service providers (ISPs) both deliver internet access, often to the same consumers. Yet their tax and regulatory treatment differ sharply. ISPs operate under the general corporate tax regime, paying as low as 20 percent corporate income tax, or 27.5 percent for unlisted entities. In contrast, mobile network operators face a sector-specific corporate tax rate of 40 percent to 45 percent.

The disparity extends to consumers. Mobile internet users pay an effective indirect tax of approximately 39 percent, while broadband customers pay only 5 percent VAT. There is no connection tax for broadband services, whereas mobile subscribers are subject to a Tk 300 SIM tax.

Such differences create artificial price distortions within the same digital ecosystem. Customers of mobile operators bear a significantly higher fiscal burden for accessing comparable internet services. Over time, this uneven structure weakens incentives for nationwide mobile broadband expansion, particularly in rural and underserved areas where mobile networks are often the primary access point.

Ensuring a level playing field does not mean limiting competition or discouraging innovation. It means aligning regulatory and fiscal treatment across comparable services so that investment decisions are driven by efficiency and innovation, not structural asymmetry.

If Bangladesh seeks to build a sustainable and inclusive digital economy, regulatory coherence is essential.

PROTECT THE CONFIDENCE OF EXISTING INVESTORS

Attracting new foreign direct investment is important, but safeguarding existing investors is equally critical. Investors already present send the strongest signal to global markets. When they expand, reinvest and publicly express confidence, it enhances Bangladesh’s credibility.

Conversely, unresolved legacy issues, prolonged disputes or uncertainty over profit repatriation create caution signals internationally.

Investor confidence is shaped by experience. The long-running audit dispute between telecom operators and the Bangladesh Telecommunication Regulatory Commission illustrates the challenge.

In 2017, the BTRC initiated an audit of two large mobile operators covering the period from 1997 to 2014, a long retrospective window that unsettled long-term investors. In 2019, the BTRC claimed Tk 125 billion from Grameenphone. More than 70 percent of the claim represents late fees, making the demand largely penalty-driven, while the audit period itself was retrospective. The claim was reportedly many times higher than those faced by peer operators, based on differing methodologies within the same industry, raising concerns about proportionality and consistency.

Six years on, the matter remains unresolved. Early efforts at amicable settlement and arbitration did not proceed.

For global investors, such prolonged disputes, retrospective interpretations and jurisdictional ambiguities elevate perceived risk. Capital flows where rules are stable and enforcement is predictable.

Challenges are not limited to telecoms. The exits of multinational pharmaceutical companies such as GlaxoSmithKline Bangladesh and Sanofi Bangladesh highlight broader concerns about regulatory complexity and market sustainability.

Bangladesh’s ambition to become a high-income, digitally advanced economy will require sustained foreign investment. The capital exists globally, but competition for it is intense.

The path forward is clear: institutionalise non-retroactive regulatory enforcement, ensure time-bound dispute resolution, strengthen policy consistency and treat existing investors as strategic partners.

Bangladesh does not lack potential. It must now demonstrate predictability.

The world is watching, and capital will follow clarity.

The new government may consider structured quarterly engagement with major foreign investors, fast-track mechanisms to resolve long-pending regulatory matters, and clear frameworks for dividend repatriation and foreign currency access.

Retention is as important as attraction.

SIMPLIFY AND MODERNISE THROUGH STRATEGIC DEREGULATION

Strategic deregulation does not mean weakening oversight; it means making regulation clearer, faster and more predictable. This requires eliminating redundant approvals, overlapping jurisdictions and outdated compliance requirements that increase costs without adding value. Digitised licensing processes, single-window clearances, defined timelines and reduced discretionary interpretation would materially improve the ease of doing business.

For investors, regulatory complexity is often more damaging than taxation. Each additional approval layer, procedural ambiguity or delayed clearance raises risk premiums and slows capital deployment. A streamlined and transparent regulatory environment signals institutional maturity, reduces friction, accelerates investment cycles and strengthens Bangladesh’s competitiveness in an increasingly contested regional landscape.

Bangladesh has proven that it can deliver growth. The next challenge is to restore and strengthen confidence.

The new government has a rare opportunity to reset perceptions and send a strong pro-investment signal to global markets. Clear reforms in predictability, regulatory efficiency, dispute resolution and digital policy coherence will elevate not just one sector, but the entire investment climate.

Most foreign investors remain committed to Bangladesh’s long-term potential. But commitment requires clarity.

The time for indicative signals alone has passed. The time for structural action is now.

The writer is chief executive officer of Grameenphone

Comments