Bangladesh’s cement producers reject US ‘overcapacity’ claims

Bangladeshi cement manufacturers have dismissed claims by the Office of the US Trade Representative (USTR) last week over alleged industry overcapacity, insisting that the sector’s production reflects growing domestic demand driven by a decade of major infrastructure projects and the needs of a rapidly expanding economy.

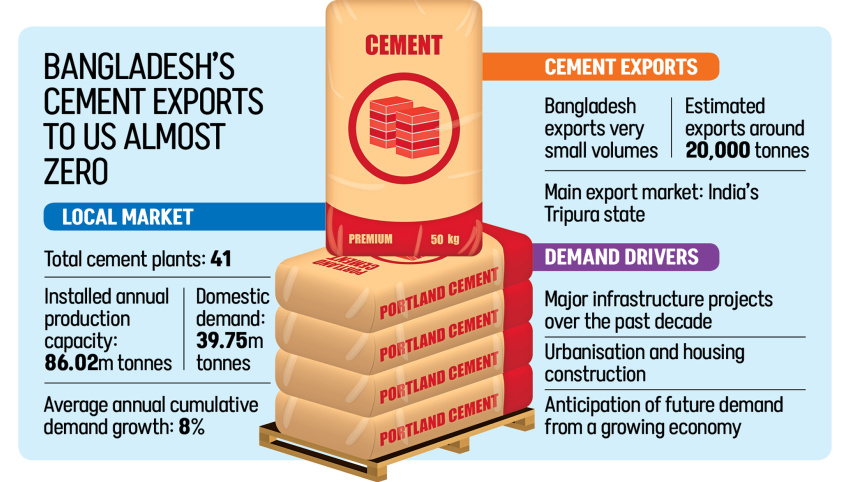

They also pointed out that Bangladesh exports very little cement, with shipments to the United States nearly non-existent. Most exports are directed to neighbouring regions of India.

The comments come amid a US trade investigation into Bangladesh and more than a dozen other economies, examining whether their policies and production practices are contributing to global overcapacity that could harm American manufacturing.

In its official complaint, the US cited unused capacity in Bangladesh’s cement industry as evidence of unfair trade.

According to the Bangladesh Cement Manufacturers Association (BCMA), the country has 41 cement plants with a combined annual production capacity of 86.02 million tonnes.

The domestic demand was at 39.75 million tonnes in 2025, up 5.55 percent from the previous year.

Multinational companies account for around 20 percent to 25 percent of this capacity. Bangladesh exports a very small amount of cement, with annual shipments to India’s Tripura estimated at roughly 20,000 tonnes, according to BCMA.

Mohammod Khourshed Alam, deputy managing director of Fresh Cement, a concern of Meghna Group of Industries, said, “Bangladesh’s cement capacity should not be interpreted simply as overcapacity, as the sector is preparing for future demand in a growing economy.”

He said that while the country’s installed capacity stands at about 86 million tonnes, annual consumption is roughly 40 million tonnes.

“Although this may appear excessive on paper, it reflects long-term planning rather than unnecessary investment,” Alam said.

He said cement demand in Bangladesh has grown at an average annual rate of around 8 percent. If this trend continues, the existing capacity could be fully absorbed within eight to nine years.

“In a country of 170 million people with ongoing urbanisation and infrastructure development, production capacity must anticipate future demand,” Alam added.

He also highlighted structural challenges, with almost all raw materials imported, leaving the industry vulnerable to global supply disruptions and shipping delays.

Demand is also highly seasonal, peaking during the dry construction months. In some periods, deliveries can reach around 4.5 million tonnes, requiring sufficient capacity to ensure an uninterrupted supply, Alam added.

Echoing a similar perspective, Mohammed Amirul Haque, president of the BCMA and managing director of Premier Cement Mills PLC, said claims of overinvestment or overproduction are misleading.

“There is no evidence of overinvestment in the industry,” he said, responding to claims linked to the US investigation. “What is often described as overcapacity actually reflects how industrial capacity is measured and utilised in practice.”

Haque said that installed capacity represents the theoretical maximum output under ideal conditions, while factories rarely operate at full capacity year-round.

Maintenance requirements, power and gas shortages, and seasonal fluctuations mean plants cannot sustain peak production continuously. Cement’s limited storage life also forces manufacturers to maintain adequate capacity to meet sudden surges in demand, he further said.

“If capacity is not built ahead of demand, the industry would struggle to supply the market during peak construction periods,” he said, adding that demand has been growing by around 8 percent to 10 percent annually, driven by infrastructure development, housing projects, and urbanisation.

Mohammad Iqbal Chowdhury, chief executive officer of LafargeHolcim Bangladesh PLC, said the sector has expanded significantly over the past 15 years in anticipation of sustained infrastructure investment.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Chowdhury said Bangladesh exports very little cement, with shipments to the US almost nil. Limited exports mainly go to India.

“For that reason, it is difficult to see how the overcapacity of Bangladesh’s cement industry is linked to the US market,” he said, adding that the sector’s surplus reflects long-term investment decisions by local companies anticipating continued infrastructure growth.

Md Moshiur Rahman, chief executive of Akij Resource, which oversees Akij Cement, said the country’s cement capacity should be understood in the context of long-term development needs.

With per capita cement consumption at around 210 kilograms, far below China’s 1,700 kilogrammes and roughly half of India’s, he said there is substantial room for growth as urbanisation and infrastructure expansion continue.

He also mentioned the presence of multinational companies such as LafargeHolcim, Heidelberg Materials, and Thailand’s INSEE, which together account for around a quarter of total production.

Comments