Capital position of Bangladeshi banks turns negative

Bangladeshi banks have emerged as the weakest in South Asia in their ability to absorb financial shocks, after a large volume of previously hidden bad loans came to light following the fall of the Awami League-led government in August 2024.

As these losses surfaced, capital buffers of banks were eroded, pushing their capital adequacy ratio into negative territory by the end of 2025, according to Bangladesh Bank’s latest Financial Stability Report yesterday.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The capital adequacy ratio, also known as the Capital to Risk-Weighted Assets Ratio (CRAR), measures how much money a bank holds as a safety cushion against risky lending. In simple terms, it shows whether a bank has enough capital to absorb losses if borrowers fail to repay loans. A negative ratio means losses have wiped out that buffer entirely.

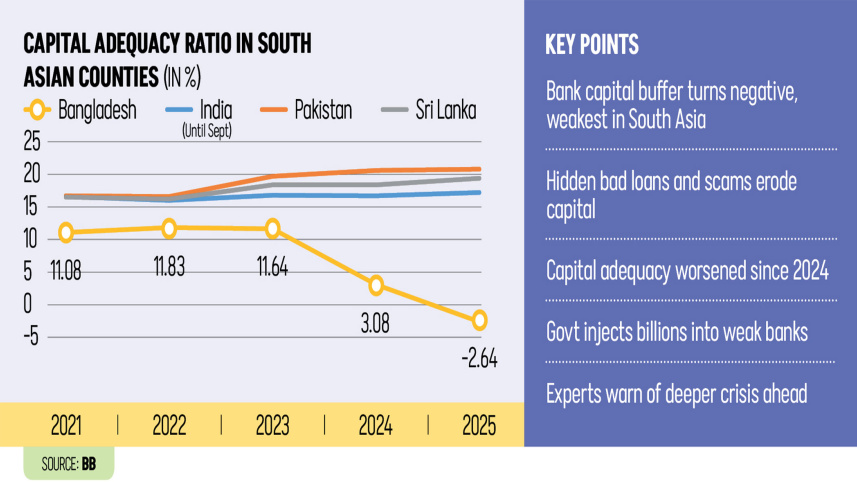

At the end of 2025, Bangladesh’s CRAR stood at minus 2.64 percent. By comparison, it was 17.20 percent in India as of September last year, 19.40 percent in Sri Lanka, and 20.80 percent in Pakistan at the end of 2025.

Under international Basel III rules, banks are expected to maintain a minimum capital adequacy ratio of 10 percent, plus an additional 2.5 percent buffer to protect against financial stress. Bangladesh is now far below that threshold.

The central bank report shows that Bangladesh’s banking sector was relatively stronger until 2023, but its financial position deteriorated drastically from 2024 after the political changeover.

In 2024, the sector’s capital adequacy ratio stood at 3.08 percent, compared with 16.7 percent in India, 20.6 percent in Pakistan and 18.4 percent in Sri Lanka.

Banking sector insiders say the collapse shows years of irregularities and large-scale financial scams during the Awami League government, which led to massive losses that were not fully disclosed at the time.

Syed Mahbubur Rahman, managing director and chief executive officer of Mutual Trust Bank and a former chairman of the Association of Bankers, Bangladesh (ABB), said the capital position of the banking sector has turned negative due to widespread financial scams.

According to Rahman, a number of banks have also availed themselves of regulatory deferral facilities. These are temporary measures that allow banks to delay recognising losses or meeting certain regulatory requirements, often used to ease short-term pressure on their balance sheets.

He said the situation could worsen further once these facilities are withdrawn or expire.

Bangladesh’s banking sector has long operated with lower capital levels than its regional peers, averaging around 11 percent in recent years. However, the ratio saw a steep decline of more than 8.5 percentage points from 11.64 percent a year earlier to minus 2.64 percent at the end of December 2025.

At the end of 2025, some 42 banks remained compliant with Basel III requirements, together accounting for more than 60 percent of total banking sector assets, according to the report.

It said the overall decline was driven mainly by weak capital positions in Islamic private commercial banks, specialised development banks and several state-owned banks.

Non-performing loans (NPLs), loans on which borrowers have stopped making repayments, were the central pressure point.

At the end of last year, bad loans in the sector stood at Tk 557,217 crore, or 30.60 percent of total loans. By March this year, the amount had risen further to Tk 588,704 crore, or 32.26 percent, according to Bangladesh Bank data.

Mustafa K Mujeri, executive director of the Institute for Inclusive Finance and Development (InM) and a former chief economist of the Bangladesh Bank, said the negative capital adequacy ratio pointed to deep structural weaknesses in the sector.

“The latest figures indicate that the sector’s health has deteriorated further compared to previous years. The problems are becoming increasingly severe and harder to resolve,” said Mujeri.

He added that the scale of damage has built up over many years.

“If policymakers want to restore the banking sector to a healthy and sustainable position, there is no alternative to taking strong and decisive corrective measures,” said the former BB economist.

Meanwhile, Mutual Trust Bank CEO Rahman said the current government has taken office at a difficult time, with the financial sector’s weakness adding to its challenges. “Therefore, the government must take the matter seriously. There appears to be no alternative to recapitalisation, but the government itself lacks the necessary funds.”

Recapitalisation refers to the process of injecting fresh capital into banks to restore their financial stability after losses. In practice, it usually involves government support or mergers between weak lenders.

In his budget speech last week, Finance Minister Amir Khosru Mahmud Chowdhury said that the government is spending around Tk 40,000 crore in the current fiscal year to recapitalise weak banks to restore discipline and stability in the banking sector.

He said Tk 20,000 crore of that amount was allocated to Sammilito Islami Bank, formed through the merger of five troubled lenders.

Rahman said broader structural reforms, including bank mergers and other resolution mechanisms, would be needed to stabilise the sector.

He pointed to Greece as an example of a country that faced a similar banking crisis but managed recovery through large-scale recapitalisation backed by the European Union.

Bangladesh, he added, does not have the same fiscal capacity.

Comments