Economic risk rises despite political clarity

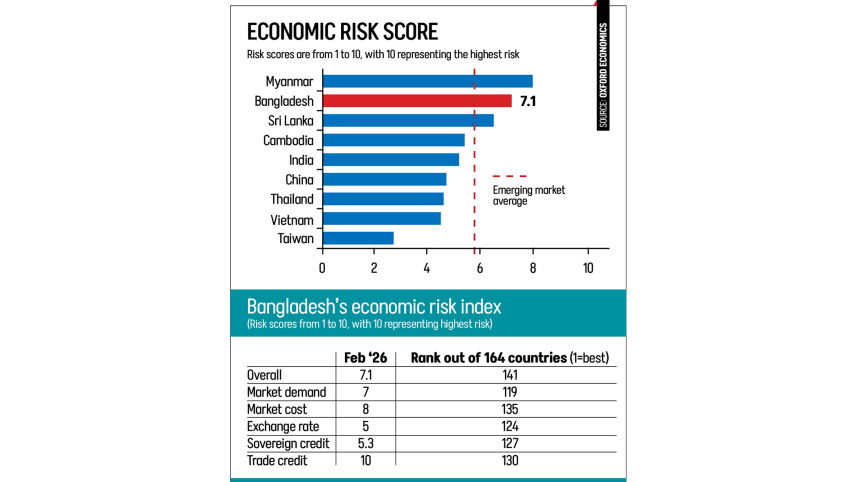

The overall economic risk of Bangladesh has increased by 0.4 points since August last year to 7.1, even as political clarity returns following the national election this month, according to Oxford Economics.

With the latest score above the Asia-Pacific average of 5.1, the country now ranks 141st out of 164 economies on its global risk index.

The report says that while the smooth election process has helped reduce political uncertainty and should support confidence in the near term, macroeconomic stability has weakened in recent years, and growth is expected to improve only gradually.

Oxford Economics, a leading global independent economic advisory firm, measures risk on a scale of 1 to 10, with 10 indicating the highest level of vulnerability.

It says trade credit risk remains the most significant vulnerability of Bangladesh, receiving the maximum score of 10, reflecting high non-performing loans (NPLs), especially in state-owned banks, alongside governance weaknesses and limited credit information.

Market costs are also elevated, driven by high interest rates and financing constraints, while demand conditions, sovereign creditworthiness and exchange rate pressures continue to weigh on the overall risk profile.

Although the exchange rate regime has moved towards greater flexibility, the taka continues to be managed within a relatively narrow band through intervention. Further reforms are expected under the International Monetary Fund (IMF) programme.

The report, titled “Political Clarity Returns but Transition Risks Linger”, says that the decisive electoral victory of the Bangladesh Nationalist Party (BNP) has restored a degree of political clarity.

However, it notes that macroeconomic stability remains fragile and the recovery path uneven.

According to the report, the new government faces several immediate challenges, such as rebuilding investor confidence, strengthening revenue mobilisation, navigating the post-LDC trade transition and maintaining stability under restrictive monetary conditions.

Moreover, Bangladesh’s debt remains in speculative grade territory, while climate vulnerability continues to pose long-term fiscal risks.

Political uncertainty may have eased, but structural weaknesses and reform risks continue to shape the outlook.

GROWTH OUTLOOK SOFTENS

Reflecting weaker trade performance and persistent inflation, Oxford Economics has downgraded its GDP growth forecast for Bangladesh for FY 2025-26 to 4.5 percent from 4.7 percent earlier.

Growth is projected to recover to 5.7 percent in FY 2026-27, although this would still be modest by Bangladesh’s historical standards, where annual growth has averaged about 5.8 percent since the mid-1990s.

The economy expanded by 4 percent in FY 2024-25, marking its weakest performance in decades outside the pandemic period, amid political unrest, floods and subdued external demand.

The report says inflation continues to weigh on the economic recovery of Bangladesh.

After easing briefly, price pressures have intensified again. In January, inflation rose to 8.6 percent year-on-year, up from 8.2 percent in October and still above the 7 percent level the Bangladesh Bank has set as a condition for policy easing.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. The central bank has kept the policy rate unchanged at a restrictive 10 percent in an effort to curb inflation and rebuild foreign exchange buffers.

Wage growth, at around 8 percent, remains below inflation, eroding real purchasing power and limiting consumer demand.

Strong remittance inflows, which grew 32 percent year-on-year during November to January, have offered partial support to households, although medium-term flows remain vulnerable to Gulf economic conditions and oil price movements.

EXTERNAL PRESSURES MOUNTING

The export sector, heavily reliant on ready-made garments, has faced renewed headwinds.

After a temporary rebound in the third quarter of 2025, exports declined sharply in the fourth quarter as earlier order frontloading in the United States faded and demand in Europe weakened.

Shipments to both the United States and Germany, each accounting for more than one-fifth of total exports, contracted notably.

While lower US tariffs and a new trade deal could provide short-term relief, Bangladesh’s upcoming graduation from least developed country status in November 2026 presents a major medium-term challenge.

The European Union and the United Kingdom together absorb roughly 60 percent of Bangladesh’s merchandise exports, most of which currently enter duty-free under the Everything but Arms (EBA) arrangement.

Following graduation, exports could face tariffs of between 9 percent and 12 percent, potentially eroding competitiveness.

Oxford Economics warns that while some export frontloading may occur ahead of the transition, the eventual loss of trade preferences poses a significant risk to medium-term export prospects.

EXTERNAL BALANCE MAY WEAKEN AGAIN

The current account returned to surplus in 2025, supported by strong remittances and reduced profit outflows.

However, Oxford Economics expects it to revert to a narrow deficit in 2026 as imports recover and export growth slows.

Foreign exchange reserves have improved to around $22 billion from roughly $17 billion in 2024, aided by tight monetary policy and IMF support.

Even so, reserves still cover only about four months of imports, leaving the economy exposed to external shocks.

Comments