AB Bank pivots to SMEs amid recovery push

AB Bank has made a decisive strategic shift toward micro, small and medium enterprises (MSMEs), moving away from its earlier concentration in large corporate lending, said Reazul Islam, acting managing director and CEO.

The move by the oldest private commercial bank of the country is a recalibration amid a weak economic environment marked by subdued private sector demand and geopolitical uncertainties, he told The Daily Star in a recent interview.

“Excessive concentration in large corporate exposures historically created vulnerabilities,” Islam said.

By distributing loans across a broader base of smaller borrowers, the bank aims to reduce systemic risk -- ensuring that isolated defaults do not significantly undermine overall stability.

“While corporate lending will continue, it will be more selective, with greater emphasis on supporting strong existing clients rather than pursuing aggressive expansion.”

Digital transformation sits at the heart of the bank’s new direction, according to Islam, a veteran banker with 29 years of experience in regulatory management, banking and professional services, who joined the bank in August 2024 as additional managing director.

He informed that AB Bank is developing fully branchless, digital loan processing systems and plans to introduce nano loans pending regulatory approval.

It is also deploying AI-based credit assessment tools and automated decision-making to minimise human intervention and move toward instant, paperless loan approvals via mobile platforms.

By leveraging alternative data sources, such as transaction behaviour and digital footprints, the bank aims to enhance credit scoring accuracy, reduce operational costs, and mitigate risk.

Over time, this digital lending framework is expected to expand beyond personal loans into SME financing, Islam said.

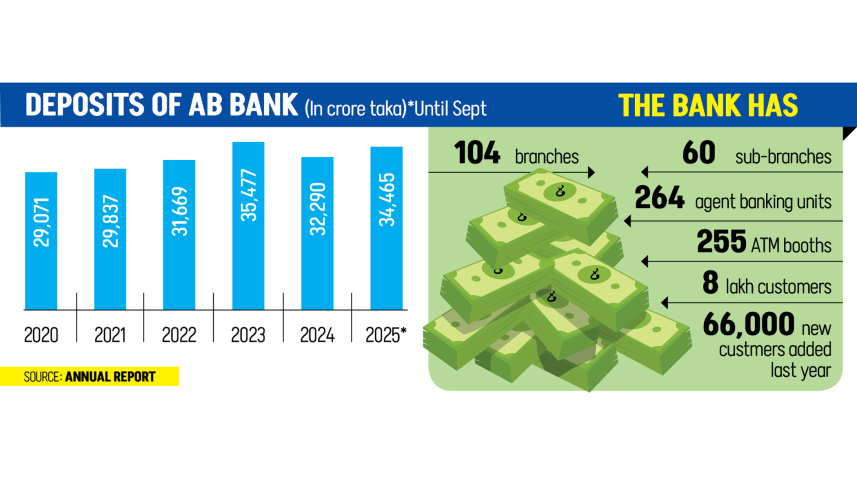

He acknowledged that the bank has lagged behind peers in agent banking and sub-branch reach, with 264 and 60 outlets respectively. “This was largely due to earlier strategic decisions and delayed entry into these segments.”

Both channels are now prioritised for deposit mobilisation and customer outreach, with new expansion targets set, though regulatory approvals remain a constraint.

Approaching 44 years since its founding in April 1982, it has faced repeated cycles of stress from the 1980s through the 2000s but demonstrated resilience by recovering from setbacks.

“This resilience has largely been driven by strong customer confidence, brand loyalty, institutional trust, and the commitment of its workforce,” says Islam.

The bank is currently navigating another difficult phase of high non-performing loans and mounting losses. Yet customers have continued to access their funds without disruption -- a factor Islam credits as critical to preserving confidence.

He says, “Liquidity management at the branch level remains relatively stable, and conditions have gradually improved.”

Islam notes that the deposit situation was particularly strained in 2024, when panic withdrawals amid broader sectoral uncertainty pushed liquidity under pressure. Total deposits fell roughly 9 percent that year to Tk 32,292 crore. The bank responded by ensuring uninterrupted cash availability and reinforcing employee confidence.

The effort paid off. Deposits recovered to Tk 34,465 crore by September 2025, with liquidity pressures easing and customer confidence gradually returning. Support from the central bank was instrumental during the peak of the crisis.

Islam, however, notes that structural challenges persist. Many loans have been rescheduled or placed under moratoriums, with repayment delays stretching up to two years -- meaning meaningful cash inflow improvements are unlikely before 2027-2028.

The bank has set targets to reduce NPLs by 20-25 percent in the near term and 30-40 percent over time, and has engaged international asset recovery firms to trace and reclaim overseas assets linked to defaulted loans.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. “While this is a time-intensive process, early indications suggest some progress,” says the bank’s CEO.

On costs, the bank is targeting a 25 percent year-on-year reduction and has already achieved around 15 percent savings in recent quarters.

The private bank’s overall recovery plan spans three to five years -- from 2025 through 2027 and beyond -- and a longer-term vision extending up to a decade.

The timeline remains contingent on external economic conditions and policy support, but the direction is clearly focused on rebuilding stability and strengthening fundamentals.

Islam says the strategy is built around digital transformation, SME-focused lending, cost efficiency, deposit growth, and improved governance.

In terms of shareholder returns, he notes that the bank is not in a position to pay dividends in the near term due to its current financial condition.

Management remains focused on restoring profitability and operational stability before resuming dividend payments, he adds.

The managing director described the current board of the bank as professional and supportive, with decision-making processes aligned with management priorities.

While acknowledging that governance issues may have contributed to past challenges, he emphasised that ongoing reforms are focused on strengthening transparency, accountability, and professionalism.

Comments