BB eases lending limits for big businesses

The Bangladesh Bank (BB) has temporarily loosened the rules so commercial banks can lend more to big borrowers, treat trade guarantees more lightly, and adjust large loan limits based on how healthy their loan books are.

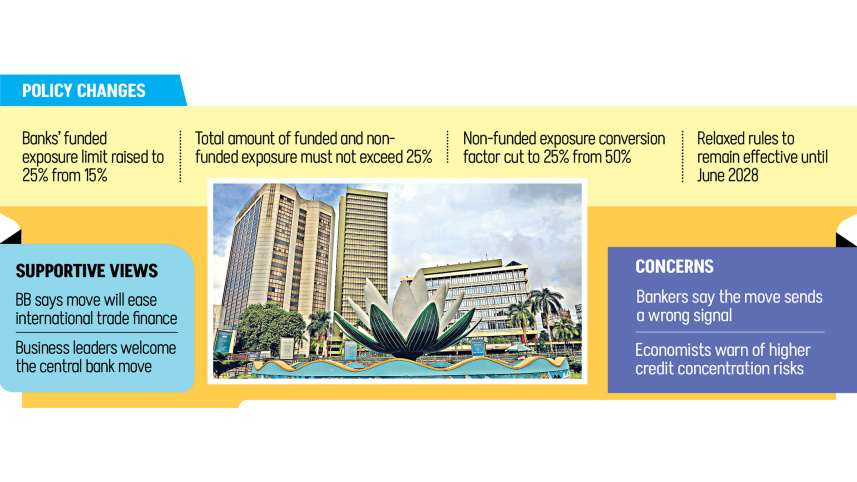

In a circular issued yesterday, the banking regulator said commercial lenders may lend up to 25 percent of their capital to a single client or group until June 2028. This is 10 percentage points higher than the existing ceiling of 15 percent.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Besides, non-funded exposures, such as letters of credit (LCs), will be weighted at just 25 percent until mid-2027, down from the current 50 percent.

At the same time, banks will be allowed to extend higher large-loan limits depending on their classified loan ratios.

In the circular, the central bank said the changes are meant for easing international trade finance for businesses and industries.

However, several BB officials said the facility came after a few large industrial groups exceeded their exposure limits at a number of banks.

Business leaders welcomed the decision by the BB, but economists and bankers were critical of the move. They said that looser rules could concentrate credit further in the hands of a small number of large conglomerates and politically connected economic actors.

NEW EXPOSURE LIMITS

Under the relaxed rules, banks will be allowed to extend funded loans of up to 25 percent of their total capital to a single borrower, up from the existing limit of 15 percent.

However, the combined exposure of funded and non-funded facilities must not exceed 25 percent under any circumstances, the central bank said.

Under the new rules, the conversion factor for non-funded exposure has been reduced to 25 percent from 50 percent. This means banks will now count only 25 percent of their total non-funded exposure when calculating large loan limits.

The facility will remain in place until June 30, 2027. The conversion factor will then increase in phases, rising to 30 percent by December 31, 2027; 40 percent by December 31, 2028; and 50 percent by December 31, 2029.

As per the single borrower exposure rules, a borrower may take up to 25 percent of a bank’s capital in total exposure, including both funded and non-funded facilities. Of this, 15 percent may be funded exposure and 10 percent non-funded exposure.

Previously, funded loans were capped at 15 percent of a bank’s capital. Under the new rules, banks may extend funded loans of up to 25 percent, but only if no non-funded exposure is provided. If funded exposure stands at 20 percent, a further 5 percent may be non-funded exposure.

For example, an LC worth Tk 100 was previously converted into funded exposure at Tk 50. Under the new framework, only Tk 25 will be counted.

The central bank has also revised limits on large loans based on banks’ classified loan ratios.

Under the previous rules, banks with classified loans of up to 3 percent could extend large loans amounting to 50 percent of their total loans and advances. Under the new rules, this threshold has been extended up to 10 percent.

Banks with classified loans between 10 percent and 15 percent may now maintain large loans of up to 46 percent of total loans and advances. Those with ratios between 15 percent and 20 percent will be allowed up to 42 percent, while banks in the 20 percent to 25 percent range may go up to 38 percent. For those between 25 percent and 30 percent, the ceiling will be 34 percent.

Where classified loans exceed 30 percent, large loans will be capped at 30 percent of total loans and advances.

The central bank has also raised the overall ceiling for large loans to 600 percent of a bank’s capital, up from 400 percent.

WAS IT NECESSARY NOW?

Several central bank officials, speaking on condition of anonymity, said a few large industrial groups have exceeded their exposure limits at several banks. The facility has been introduced in response to their requests.

A managing director of a commercial bank, who asked not to be named, said the current condition of the banking sector is not good.

“So, this kind of forbearance was not necessary at this time,” he said, adding that it sends the wrong signal and is contrary to international standards.

However, Mir Nasir Hossain, former president of the Federation of Bangladesh Chambers of Commerce & Industry (FBCCI), welcomed the central bank’s move.

He said the economy has expanded and many large companies often need consortium financing.

“Increasing the exposure limit will be beneficial for trade and business. It is a business-friendly decision,” said Hossain.

Ashikur Rahman, principal economist at the Policy Research Institute of Bangladesh, took a different view.

“At a time when concerns over governance, non-performing loans, and weak risk management already plague the banking sector, such relaxation may deepen systemic vulnerabilities rather than strengthen financial intermediation,” Rahman told The Daily Star.

He said that excessive concentration of lending not only undermines diversification of bank portfolios, but also amplifies the “too-connected-to-fail” problem within the financial system.”

The economist argued that a more prudent long-term approach would gradually steer large borrowers towards corporate bond issuance and capital market financing, reducing reliance on banks for major industrial projects.

“Deepening the bond and equity markets is essential if Bangladesh wishes to build a more balanced and resilient financial architecture. Unfortunately, this decision appears to move in the opposite direction, reinforcing existing distortions instead of correcting them,” he commented.

Comments