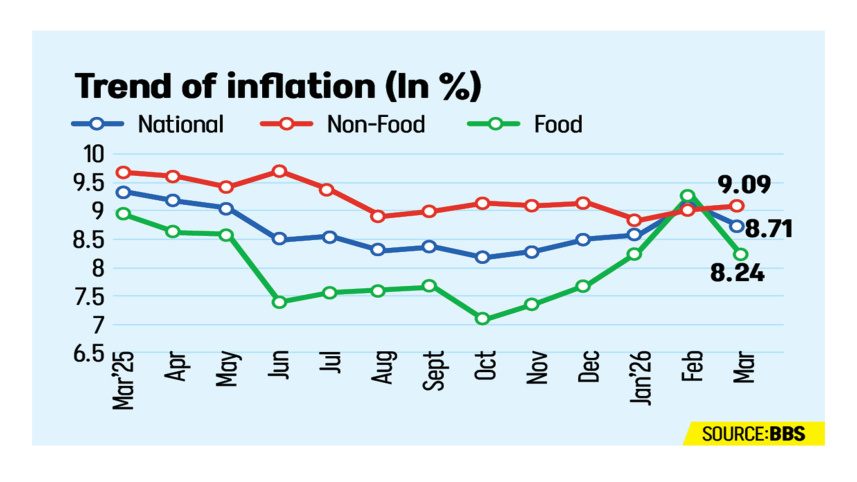

Inflation eases to 8.71% in March, but war-induced risks persist

Inflation eased to 8.71 percent in March, offering slight relief to consumers, but analysts warn that prices may remain sticky in the coming months as the US-Israel war on Iran drives up costs and disrupts supply chains.

Food price inflation fell to 8.24 percent from 9.3 percent the previous month, according to data released yesterday by the Bangladesh Bureau of Statistics. Non-food inflation, however, edged up to 9.09 percent from 9.01 percent in February.

The moderation follows a spike to 9.13 percent in February, a ten-month high, when higher food prices ahead of Ramadan and increased election-related spending fuelled demand, pushing the Consumer Price Index.

Md Deen Islam, professor of economics at Dhaka University, said, “Food prices carry a large weight in the consumer basket, and the decline in inflation might be driven mainly by a moderation in food prices.”

Three factors -- improved supply of food due to no major climate shock, the lagged effects of relatively tighter monetary policy, and subdued aggregate demand -- may have helped contain overall price increases, he added.

However, the persistence and slight increase in non-food inflation to 9.09 percent signal that underlying cost pressures in the economy remain strong, noted the professor.

“Non-food components such as energy, transport, and imported goods continue to be affected by exchange rate depreciation and elevated global prices,” he said.

Bangladesh has been grappling with stubborn inflation for more than three years, with the burden falling hardest on poor and low-income households, who spend a disproportionate share of their earnings on food.

In March, rural inflation was marginally higher at 8.72 percent compared to 8.68 percent in urban areas.

Zahid Hussain, former lead economist at the World Bank’s Dhaka office, said food inflation above 8 percent shows that price pressures persist.

“A slight easing in March is not unusual, but it does not mean inflationary pressure has disappeared,” he said.

Birupaksha Paul, professor of economics at the State University of New York, echoed the sentiment, saying the decline in inflation is not significant. “Expected inflation is on the rise and most part of it is fear driven.”

Ashikur Rahman, principal economist at the Policy Research Institute (PRI), said the March moderation should be read with caution.

“The spike observed in February was largely driven by a temporary surge in consumption, typically associated with heightened political and electoral activity.

“Such demand-side pressures tend to be short-lived, and the subsequent correction in March reflects the dissipation of this transient effect rather than a structural easing of inflationary pressures,” he said.

The economist pointed out that the broader inflation outlook remains fragile. Rising global fuel costs from the Middle East conflict could force adjustments in administered energy prices, with direct and second-round effects on transport, production, and food supply chains.

Besides, he added, “Supply chain disruptions stemming from the conflict could elevate import costs, particularly for essential commodities, thereby feeding into domestic inflation.”

Hussain, meanwhile, noted that government-set fuel prices remained unchanged, with even an expected April adjustment deferred. “If fuel prices had been adjusted at the pump level, the impact would have shown up in the CPI,” he said. “But the impact is inevitable.”

For instance, he pointed out that the exchange rate already saw an impact in March. In the interbank market, the rate increased by nearly one taka. But the effect of that on import prices will take time -- likely showing up in April -- because payments for March imports were largely made earlier.

Prof Islam said the divergence between declining food inflation and rising non-food inflation suggests the recent improvement is narrow and not yet indicative of a broad-based disinflation.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. He expects inflation to remain relatively sticky in the near term, with the Middle East conflict posing a significant upside risk.

In this context, PRI’s Rahman said macroeconomic management must stay vigilant.

He backed Bangladesh Bank’s contractionary monetary policy stance as “necessary to contain demand-side pressures,” but added that monetary policy alone would not suffice.

“Complementary fiscal discipline and targeted supply-side interventions, particularly to stabilise food markets, will be critical in anchoring inflation expectations and safeguarding macroeconomic stability in the months ahead,” he said.

Comments