Two-thirds of agent banking outlets not engaged in lending: study

About two-thirds of agent banking outlets in Bangladesh were not engaged in lending as of December 2024, highlighting a major gap in credit delivery despite the network’s rapid expansion, a recent study has found.

Titled “Agent banking in Bangladesh: Strong expansion, some inclusion”, the research was funded by the UK-based International Growth Centre (IGC) and examines whether agent banking has translated into meaningful financial inclusion.

The study used a newly constructed dataset that collected information linked to the geographical location of agent banking outlets, developed by the Policy Research Institute (PRI), covering 2022-2024. It maps the expansion, distribution, and financial activity of agent banking outlets across Bangladesh.

Since its introduction in 2013, the agent banking network has grown from 2,601 outlets in 2016 to over 21,000 by 2024. However, recent trends suggest a slowdown, meaning expansion may be approaching saturation.

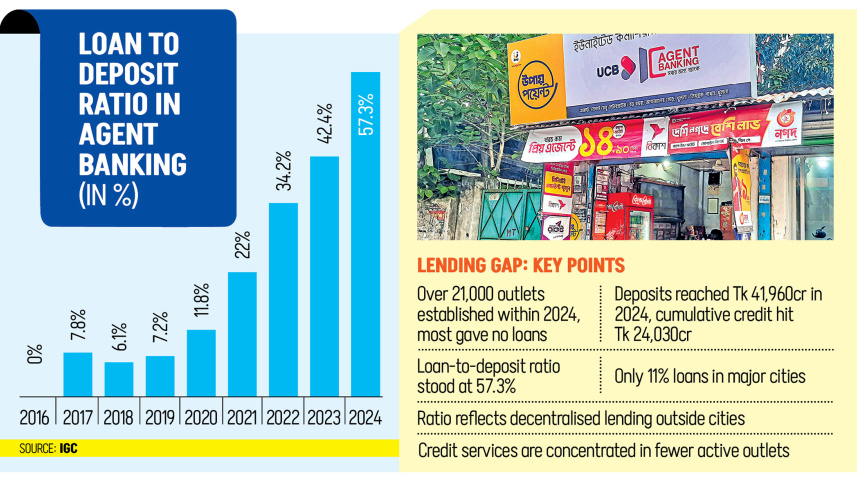

Despite growth, agent banking is more effective at mobilising deposits than providing credit, according to the study.

Deposits rose from Tk 380 crore in 2016 to Tk 41,960 crore in 2024, while cumulative credit disbursement reached Tk 24,030 crore, giving a loan-to-deposit ratio of 57.3 percent.

However, this increase in the provision of financial services is uneven and concentrated in fewer active outlets, it was found.

The research also highlights a shift in banking geography. Traditional banking is heavily concentrated in Dhaka and Chattogram, which account for around 65 percent of deposits and 78 percent of total lending.

In contrast, only about 11 percent of agent banking loans originate from these cities, showing that agent banking has helped decentralise credit flows.

Rural areas have benefited, with about 15 outlets per 100,000 people, improving access compared to traditional branch banking. Rural per capita deposits are also higher, indicating strong uptake outside urban centres.

However, credit delivery remains limited. The study identifies a “zero-loan phenomenon”, where about two-thirds of outlets had no outstanding loans in 2024, suggesting those outlets function mainly as deposit and transaction points rather than credit providers.

This is more pronounced in remote and disadvantaged regions, including the Chittagong Hill Tracts.

Outlet distribution is closely linked to existing branch density, suggesting agent banking often extends traditional banking rather than expanding independently into underserved areas.

There is also no strong evidence that poorer upazilas are prioritised, while higher literacy levels are associated with greater activity.

On gender, over 92 percent of operators are male, but women are using the system more and more. Female account growth outpaces male growth between 2022 and 2024.

“As expansion begins to slow, policy should shift from improving access to strengthening financial intermediation. This requires enabling agent-based lending through appropriate regulatory frameworks, using digital data for credit scoring, and aligning incentives so agents can serve as effective credit channels for underserved communities,” said Ashikur Rahman, principal economist at the PRI and co-author of the study.

He also called attention towards a stark gender imbalance among agents and stressed that addressing this issue must become a policy priority to ensure that financial inclusion is both deep and equitable.

The study concludes that while agent banking has significantly expanded access to financial services, its next challenge is strengthening credit intermediation, particularly in underserved and rural areas.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

Comments