What are the govt’s key deregulation measures?

The government has announced a wide-ranging deregulation programme aimed at cutting red tape, lowering compliance costs and improving Bangladesh’s business climate as the country prepares for graduation from least-developed country (LDC) status.

The reform package, unveiled in the budget speech of Finance Minister Amir Khosru Mahmud Chowdhury on Thursday, covers investment approvals, company registration, taxation, customs, banking, capital markets and construction permits.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Businesses have long complained about lengthy approval processes, overlapping regulations and cumbersome compliance requirements that delay investment decisions and raise operating costs.

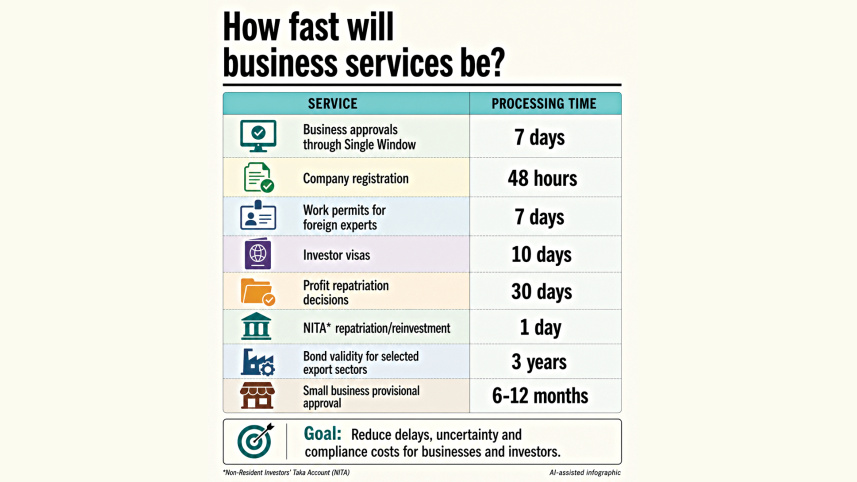

SEVEN-DAY DEADLINE FOR APPROVALS

A key feature of the reform package is the introduction of strict timelines for government approvals and licences.

The government plans to make the online Single Window platform mandatory for business approvals and licensing. From application submission to licence issuance, all procedures will have to be completed within seven days.

If a government agency fails to provide a required opinion, clearance or no-objection certificate within the stipulated period, the application may be processed on the assumption that consent has been granted, where applicable.

Authorities also plan to introduce “plug-and-play” facilities in selected industrial and economic zones, allowing investors to set up factories and begin production more quickly.

FASTER BUSINESS START-UP SERVICES

The government intends to simplify company registration by moving name clearance, application submission, fee payments and certificate issuance online. Company registration is expected to be completed within 48 hours.

Small and new businesses may be allowed to start operations with provisional approvals and complete remaining compliance requirements within six to 12 months.

Work permits for foreign experts and skilled professionals are set to be issued within seven days, while investor visas will be processed within 10 days. The government is also considering five-year multiple-entry visas for eligible investors and project personnel.

To facilitate large investments, agencies such as Bida, Beza, Bepza and BSCIC will assign dedicated support teams and case managers. A grievance redress mechanism and a 24-hour investor help desk are also planned.

TAX ADMINISTRATION GOES DIGITAL

The deregulation drive includes measures to simplify tax and VAT compliance. From the next fiscal year, corporate taxpayers will be able to file returns online, while excess tax deducted at source will be refunded directly to bank accounts through an automated system.

Tax and VAT audit selection will be automated using risk-based software, while tax residency certificates for foreign investors will be issued online through the National Single Window.

For VAT, online filing will become mandatory, simplified returns will be introduced for small businesses, and the government is considering quarterly instead of monthly VAT submissions.

CUSTOMS PROCEDURES TO BE SIMPLIFIED

Several reforms target customs administration and bonded warehouse facilities.

The government plans to extend bond facilities beyond the readymade garments sector to other export-oriented industries. Annual bond audits for compliant garment exporters may be withdrawn, while bond validity periods in some sectors will be extended.

Ten sectors, including motorcycles, speedboats, fish processing, handicrafts, diversified jute products and sanitary products, may be allowed to import raw materials against bank guarantees without obtaining bond licences.

Authorities also plan to reduce customs paperwork, expand self-assessment facilities and allow accredited private laboratories to conduct product testing alongside government facilities to reduce port congestion and delays.

EASIER PROFIT REPATRIATION

To improve investor confidence, the government intends to simplify rules governing profit repatriation and capital transfers.

Applications related to the repatriation of profits from foreign investments will be processed within 30 days. Requirements for share transfers and capital repatriation in unlisted companies will be eased, while certain transactions will no longer require prior approval from Bangladesh Bank.

The reform package also proposes simplifying foreign trade payments, expanding digital lending and cashless transactions, and easing regulatory requirements for banking services.

CAPITAL MARKET AND CONSTRUCTION APPROVALS

The government plans to streamline IPO approvals through digital platforms, reduce documentation requirements and review the possibility of direct listing for eligible companies.

Measures are also proposed to expand the corporate bond market and strengthen participation by institutional investors.

Construction, environmental and fire-safety approvals will be integrated into a single online platform. A risk-based approval system will be introduced so that low-risk projects receive faster clearances while higher-risk projects continue to undergo detailed scrutiny.

HIGH-LEVEL TASK FORCE

The government says a high-level task force will oversee implementation of the deregulation programme. A dedicated website will also be launched to track progress and allow businesses to report delays or irregularities in service delivery.

Commenting on the government’s deregulation initiatives, M Masrur Reaz, chairman and CEO of Policy Exchange Bangladesh, said the new government appears to be treating deregulation as a key reform tool for creating a more business-friendly environment.

He welcomed the approach, noting that Bangladesh’s business environment is burdened by unnecessary and outdated regulations, as well as red tape arising from weak regulatory enforcement.

Reaz said deregulation-driven reforms could involve removing redundant rules, simplifying existing regulations and allowing greater self-regulation by industry bodies such as the Bangladesh Garment Manufacturers and Exporters Association.

Such measures, he said, would reduce the time, cost and procedural burden of regulatory compliance for businesses, making government services faster, easier and more competitive.Bangladesh Chamber of Industries President Anwar-ul-Alam Chowdhury Parvez also welcomed several of the proposed measures, but questioned whether they could deliver results without deeper structural reforms.

Manufacturers remain more concerned about uninterrupted gas supply and a stable banking sector than fiscal incentives, he said.

Persistent energy shortages, rising non-performing loans, weak investor confidence and the absence of a clear roadmap for banking reforms continue to weigh on business sentiment, he noted, adding that success would ultimately depend on implementation capacity and institutional reforms.

Comments