MFS enabling money transfers — also abuses

Mobile financial services (MFS) have become a vital tool for distributing social safety net allowances, student stipends, remittances, and personal transfers.

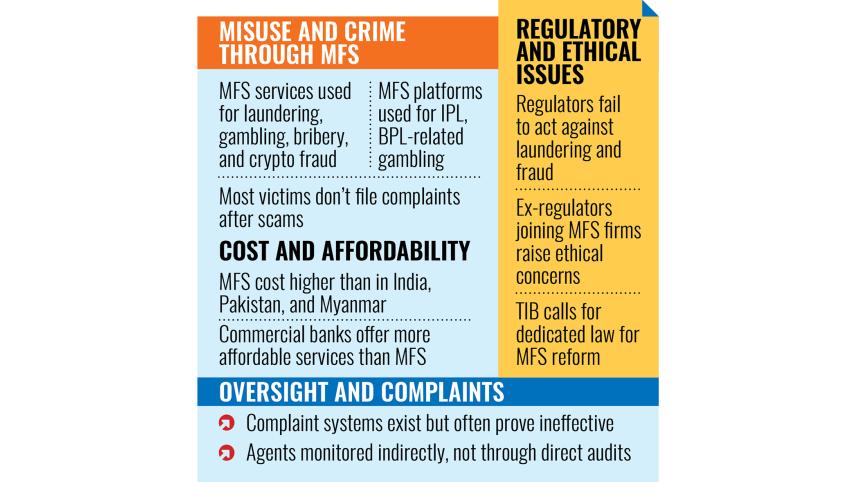

But these platforms are also being exploited for money laundering, bribery, online gambling, and illegal cryptocurrency activities, a new study has found.

The report, titled "Governance Challenges and Pathways to Reform in the Mobile Financial Services (MFS) Sector", was released yesterday by Transparency International Bangladesh (TIB).

It also found that the cost of MFS services in Bangladesh is higher than that in neighbouring countries such as India, Pakistan, and Myanmar. Traditional banking services in the country offer more cost-effective alternatives compared to MFS providers.

These findings were shared at a press conference at the TIB office in Dhaka, where its Executive Director Iftekharuzzaman spoke.

The study, conducted between November 2023 and May 2025, surveyed 1,784 personal account holders, 429 merchant account holders, and 664 agents across 32 districts.

It found that 6.3 percent of personal users, 17 percent of agents, and 1.6 percent of merchants had fallen victim to fraud or financial scams.

Of those, 3.6 percent of personal users, 8.7 percent of agents, and 1.4 percent of merchants reported monetary losses.

Losses among personal users ranged from Tk 300 to Tk 83,000. Agents reported losses between Tk 200 and Tk 3.76 lakh, while merchants lost between Tk 53 and Tk 45,000.

More than half of the victims said they were deceived by false promises of easy money or misinformation. Others were tricked through phone calls or SMS, while 12 percent lost funds due to account hacking.

Despite the monetary losses, very few took legal action. Only 7.6 percent of affected personal users, 27.4 percent of agents, and 4.2 percent of merchants filed complaints with the police or registered general diaries (GDs).

The report found widespread use of MFS for illegal betting and gambling transactions, especially during major cricket events such as the IPL, BPL, and World Cup.

Although authorities have blocked many websites and social media platforms promoting gambling, MFS operators have failed to stop related financial transactions.

Thousands of betting agents across the country collect money through MFS and transfer it abroad. Alongside traditional methods, some are using cryptocurrency to purchase US dollars, convert them to Bitcoin, and launder the funds overseas.

Citing Criminal Investigation Department (CID) data, the TIB report said around Tk 75,000 crore was laundered through MFS in 2022. As per Bangladesh Bank, remittance flows through legal MFS channels have increased as political changes curbed informal hundi networks.

Still, monitoring remains weak. MFS providers lack effective mechanisms to detect or prevent illicit transactions. The failure to permanently block accounts linked to laundering means many offenders simply re-register using new information.

The Cyber Security Ordinance, issued on May 21 this year, classifies online gambling, the development of related apps or portals, and their promotion as criminal offences.

Authorities have already identified some 1,100 MFS agents involved in such activities.

TIB also flagged unethical marketing practices among MFS providers. Some firms circulated misleading adverts and negative propaganda about competitors through leaflets, banners, and social media influencers.

Although a Police Bureau of Investigation (PBI) probe led to court summons, little action followed.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Some adverts falsely claimed service charges had been lowered, despite no actual change. Bangladesh Bank and the Competition Commission issued warnings, but regulators failed to take decisive steps, due partly to conflicts of interest and alleged corruption, according to the TIB study.

The report raised concerns over former regulators joining MFS companies, calling this a breach of ethical standards. CID had recommended action, but Bangladesh Bank remained inactive, according to the study.

While MFS companies do operate hotlines and internal complaint mechanisms, users often find them ineffective. Among those affected by fraud, 58.8 percent of personal users, 60.9 percent of agents, and 58.3 percent of merchants did not file complaints.

Of those who did, only 38.1 percent of personal users and 20 percent of merchants said their issues were resolved.

Awareness of existing protections is also low. Just 6.2 percent of surveyed personal users had heard of Bangladesh Bank's Customer Interest Protection Centre (CIPC).

The Financial Intelligence Unit (BFIU) also does not have a hotline or a clear system for reporting gambling, money laundering, or hundi-related activities.

The report found that most MFS agents are not subject to regular audits. Providers rely on third-party distributors for oversight, resulting in limited accountability.

The anti-graft watchdog called for a dedicated law to govern the MFS sector. It recommended ensuring fair competition, financial inclusion, and transparent practices.

The proposed law, according to TIB, should define stakeholder responsibilities, introduce global best practices, require service interoperability, and guarantee data protection.

TIB urged regulators to cap service charges and commissions, arrange agent training, and strengthen complaint systems.

It also called for full disclosure of contracts, strong penalties for misconduct, enhanced monitoring, and the use of advanced tools to detect suspicious transactions.

The study concluded that promoting public awareness and safeguarding consumer rights must be treated as urgent national priorities.

Comments