Vibrant bond market needed to become a developed nation

Bangladesh needs a vibrant bond market to meet its huge financing requirement for infrastructure development and further industrialisation, said a noted merchant banker.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Between 2016 and 2040, Bangladesh needs $608 billion in investment to realise its dream of becoming a developed nation, according to a report of the Global Infrastructure Hub.

But the current trend indicates there will be a shortfall of $200 billion.

“Where will the funds come from?” said Ershad Hossain, chief executive officer of City Bank Capital, one of the leading merchant banks in Bangladesh.

The onus should not entirely be on national savings certificates (NSCs) and banks.

Banks rely on short-term deposits to run operations, so when they provide long-term loans with short-term deposits it creates pressure on their liquidity management, he said.

On the other hand, the interest rate on the NSCs is too high.

“So, the government should explore other sources to mobilise funds. A vibrant stock and bond market should be the sustainable solution to the funding needs,” he told The Daily Star in an interview at his office in Dhaka last week.

At present, there are government bonds worth about Tk 200,000 crore and private bonds worth Tk 24,000 crore.

But they are not traded on the stock exchanges.

The Bangladesh Securities and Exchange Commission (BSEC) is working on stock market development so that private companies can raise funds from the market.

However, the bond market is still at a rudimentary level.

For instance, private sector bonds (corporate bond) in Bangladesh are only 1 percent of the country’s gross domestic product, whereas it is 149 percent in the US, 60 percent in China, 16 percent in India, 60 percent in Malaysia and 59 percent in Thailand.

“So, we have huge opportunity to raise funds through the bond market but the government has not attached any importance to it.”

City Bank Capital, one of the subsidiaries of the private commercial bank, has a paid-up capital of Tk 255 crore and it served as an issue manager and arranger for debt securities amounting to Tk 5,700 crore in the last three years.

Hossain also served as a director of the structured foreign exchange division at Standard Chartered Singapore where he had steered the group’s high yield bond, interest rate derivatives and complex currency structure products for the Asia Pacific region.

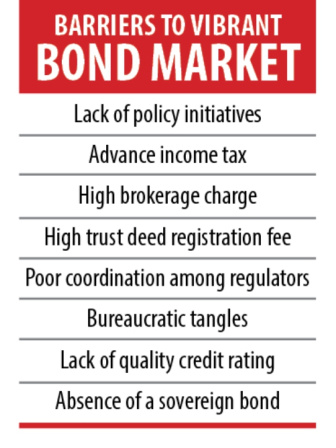

A lack of policy initiatives and awareness is the main reason behind the lacklustre growth of corporate bond issuance.

“The country’s investors lack financial knowledge, especially about the bond market.”

Another reason for the lacklustre bond market is the higher interest rate offered by the NSCs. “This creates distortion in the stock market, bond market and any other securities market.”

Hossain, who has 24 years of experience in multi-asset financial and capital market products, said the time has come to persuade investors not to put their money only with NSCs.

Only pensioners and some individuals with special needs should get higher benefits of the NSC.

“Others should not get the same interest rate and should be paid lower rate than the bank interest rate and bond premium rate.”

People can buy bonds from the over-the-counter market but they should be tradable on the stock exchanges.

“Then it will be a versatile way to get funds from general investors and to raise money easily,” said Hossain, who obtained MBA from the Institute of Business Administration under the University of Dhaka.

However, there are several impediments to trading bonds in the secondary market and one of them is advance income tax (AIT).

Hossain said when investors gain the interest on bond they should be charged income tax on it and not at the time of investment.

“So, AIT should be withdrawn to attract investors to bonds.”

The brokerage charge for the trading of bond should also be reduced as the amount of bond trading is much more than the shares of a company trading, he said.

Bond issuers also have to pay 2 percent of the bond size to the National Board of Revenue as a trust deed registration fee, which fuels the bond issuance cost.

“The BSEC has addressed the issue and it should be solved very fast.”

Apart from removing these impediments, a tax incentive is needed to boost the bond market. Primarily, tax rate can be reduced or a tax exemption can be provided to issuers and investors so that entrepreneurs and people get attracted.

“When the market develops the NBR will get more tax, but if it remains lacklustre the NBR will get nothing.”

To remove the obstacles caused by the AIT and promote incentives, coordination among all the regulators should be ensured and bureaucratic red tape should be cut, Hossain said.

Credibility of credit rating agencies is important for a vibrant bond market as the rating will determine the bond’s risk premium over risk-free rate, said Hossain, the former head of financial institutions and margin trading sales of American Express Bank in Singapore.

“So, the accountability and quality of credit rating agencies should be ensured.”

To enhance public participation in the bond market, the credibility of the financial reports of bond issuers should be confirmed.

He said many foreigners want to invest in Bangladesh not in the form of foreign direct investment but through bonds, so the government should issue a sovereign bond.

“A sovereign bond will help local businesses to issue private bonds in the offshore market.”

A country is benchmarked when it issues sovereign bond and without the benchmark corporate bond issuance at international level is quite tough.

Sovereign bonds look costlier than soft loans from development partners but the former is less strict when it comes to meeting conditions.

The government may think that if the country issues a sovereign bond, it will not get concessional loans from development partners, he added.

Comments