Banking outlook bleak

State-owned commercial banks continue to be plagued by poor capitalisation, weak asset quality and substandard management quality despite several attempts by the government to reform the sector, according to a recent analysis.

They are also burdened by obligatory lending towards priority sectors and other state-owned enterprises as well as corruption and political patronage, said BMI Research, a London-based research firm.

The report said Bangladesh's banking sector is one of the weakest in emerging Asia, as factors, such as low capital adequacy and poor asset and management quality, continue to challenge solvency and profitability.

Under the Basel III framework, Bangladeshi banks are legally required to maintain a capital to risk-weighted asset ratio (CRAR) of at least 10 percent and a tier 1 capital ratio of at least 5.5 percent.

Although the banking sector as a whole was able to maintain its CRAR above the minimum requisite, state-owned commercial banks and developmental financial institutions or specialised banks have not been compliant, it said.

Moreover, the banking sector's aggregate CRAR has been on a downtrend since 2013 and stood at just 10.3 percent in June 2015, which is slightly above the minimum requirement.

"Given the high tendency for loans to turn sour in Bangladesh, this could pose downside risks to financial stability."

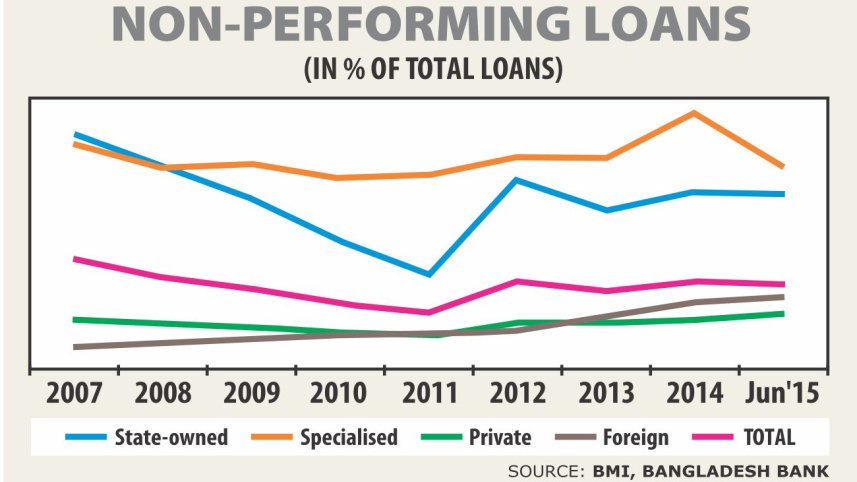

The report also said Bangladesh has one of the highest non-performing loan ratios in the region.

Although the overall NPL ratio in the sector dropped from 10 percent in December 2014 to 9.7 percent in June 2015, it has been on a broad rising trend since 2011.

"Over the coming quarters, we believe that NPLs will continue to stay elevated as a large portion of these bad loans lies within the state-owned and specialised banks, which have traditionally been inefficient in their operations."

The research firm said one of the key weaknesses of Bangladesh's banking system lies in the poor management quality, which has resulted in inefficiencies and high cost of operation.

Although management quality is largely based on qualitative aspects rather than quantitative indicators, the expense-to-income ratio can be used as proxy to measure the efficiency of the management and its soundness.

The expense-to-income ratios of the state-owned and specialised banks are higher than the private and foreign commercial banks, and the overall indicator has been on the rise since 2011.

Despite various efforts by policymakers to turn around the poorly managed state banks -- such as privatising them, converting them into limited liability companies and appointing new management -- progress has been slow, the report said.

The profitability and earning ability of Bangladesh's banking sector has been declining over the past few years.

For instance, in June last year, return on assets (ROA) and return on equity (ROE) stood at a low 0.5 percent and 6.6 percent respectively.

To put this in context, the ROA for Filipino banks averaged around 1.2 percent in the third quarter of fiscal 2015, while ROE was reported at around 10.1 percent.

"We see little prospect of this trend reversing over the coming quarters."

Due to rising levels of NPLs, banks will be forced to increase their loan-loss provisions, which will weigh on their profitability.

Furthermore, the rising level of excess liquidity in the banking sector underscores a lack of profitable lending opportunities as well as the poor business environment in the country, the report said.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Excess liquidity, as defined by cash held by a bank above what is required by the regulatory authorities, rose to 16.9 percent in June 2015 from just 6 percent in 2010, it said.

Meanwhile, the loan-to-deposit ratio fell to 71.9 percent from 79.4 percent in 2014.

"Over the coming quarters, we believe that this situation will persist as the rise in domestic security threats will continue to curb investor appetite and weigh on credit growth," the report added.

Comments