At 43, UCB is rebuilding from the inside out

United Commercial Bank PLC (UCB) turned 43 on June 26. Incorporated in Bangladesh in 1983, the bank has grown into one of the country’s largest first-generation private commercial banks. In the four decades since, it has operated through multiple changes of government, the Asian financial crisis, the global meltdown of 2008, a currency crisis, and a pandemic.

Yet the bank’s more consequential test has been recent and internal -- a prolonged period of political interference and governance failure that the current leadership is now trying to put firmly behind it.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel.

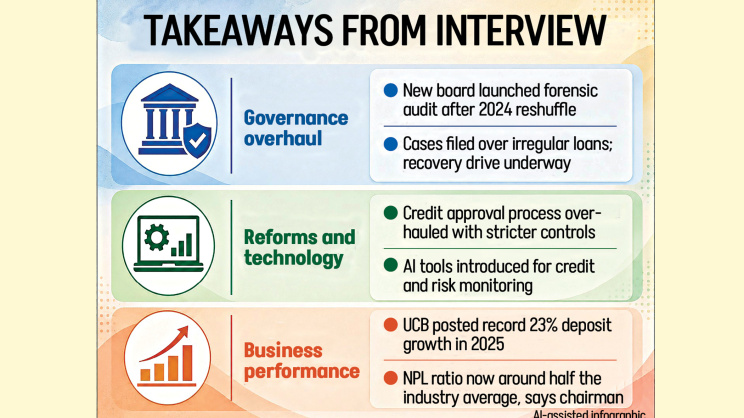

The latest rebuilding push comes after Bangladesh Bank reconstituted UCB’s board in August 2024, following the political changeover. Sharif Zahir -- former vice chairman and son of one of the bank’s founding members who was reportedly shot dead over a board dispute -- was made the new chairman.

At the time, the bank’s profit stood at Tk 8 crore, down from Tk 219 crore the year before. Its non-performing loan (NPL) ratio was at 14 percent. A massive rebuilding was necessary.

“We did not want cosmetic numbers,” Zahir says. “We wanted clarity.”

Since 2018, UCB had been heavily influenced by former land minister Saifuzzaman Chowdhury Javed and his family. A group of shareholders had alleged that although Saifuzzaman’s wife Rukhmila Zaman served as chairperson, it was the minister who pulled the strings. Loans were disbursed to shell or fictitious business entities, where the borrower on paper was often not the true beneficiary of the funds. In some cases, individuals appear to have had their identities used without their knowledge or consent.

“Financial fraud through shell or fictitious entities usually occurs only when multiple lines of defence fail at the same time,” Zahir says, pointing to failures related to documentation, approval, disbursement, monitoring, and internal audit.

Branches were often the “execution points” for the irregularities, but Zahir says “they were not always the root cause”.

“Governance is a chain. Weakness at any level -- branch, regional office, corporate office, management, board, audit, or regulatory supervision -- can create institutional vulnerability,” the UCB chair notes.

The new board moved quickly to address this. Independent forensic auditors were engaged to identify irregular exposures, trace the ultimate beneficiaries, quantify losses, and establish responsibility.

Where borrower identities appear to have been misused, the bank is working to distinguish between the legal borrower on paper and the true economic beneficiary. The move is aimed at ensuring that “innocent individuals are not unfairly burdened if they did not receive or benefit from the funds.”

Cases have been filed against those identified as responsible. A dedicated legal panel is in place, and recovery drives are ongoing.

“Recovery has several dimensions,” Zahir says. “There is cash recovery, legal recovery, collateral recovery, recovery from wilful defaulters, recovery of misappropriated assets, and recovery of confidence. We are pursuing all of them.”

UCB has also taken concrete steps to recover misappropriated money, including from abroad where applicable.

The credit governance framework has been overhauled in parallel. Business origination, risk assessment, credit administration, and approval authority are now separated into distinct functions. Every proposal must pass through structured due diligence, financial analysis, compliance checks, documentation review, and management recommendation before approval.

The bank is also deploying AI-driven credit analytics and risk management tools to detect anomalies earlier and reduce subjectivity. “The objective is to make the credit process more transparent, traceable, and data-driven,” Zahir says.

At the branch level, the bank has increased central oversight of high-risk transactions, strengthened maker-checker controls, expanded internal audit coverage, and is moving toward end-to-end digitisation to improve traceability. “Technology allows us to move from reactive supervision to real-time supervision,” Zahir says.

“During one of the most challenging periods for the industry, UCB’s deposit base crossed Tk 70,000 crore,” Zahir says. “That is a powerful signal of confidence from our customers.”

In 2025, UCB posted its highest-ever deposit growth of 23 percent, more than double the banking sector’s average of 11 percent. The bank added around 678,000 new customer accounts during the year. Its loan-to-deposit ratio fell from 91.3 percent to 83 percent, significantly strengthening its liquidity position. It recovered around Tk 114 crore from classified and written-off loans, nearly three times the amount recovered the year before.

“A major moral hazard had developed in the market when borrowers saw others not repaying,” Zahir says. “Our management team has taken a strong position to reverse that culture.”

The NPL picture is also showing improvement. The board had not declared any dividend for 2024, directing the entire operating profit toward NPL provisions instead.

“The June (2025) closing numbers have begun to show improvement, supported by stronger recovery discipline and Bangladesh Bank’s assistance in restructuring or rescheduling genuine borrowers where appropriate,” says Zahir. “Despite legacy stress, UCB’s NPL position is approximately half of the industry average.”

On capital adequacy, the bank has approached shareholders through its annual general meeting for a rights issue and is awaiting approval from the Bangladesh Securities and Exchange Commission. Once completed, UCB intends to engage strategic investors, including development finance institutions, through a professionally managed process.

“Such investors will not only contribute capital,” Zahir says. “They can bring long-term strategic value in governance, technology, risk management, and international best practices.”

Technology has been another area of focus. UCB launched what it describes as the country’s first microservices-based Open API banking platform, alongside its UCB One app. Nearly 65 percent of the bank’s total transactions are now conducted through digital channels.

Agent banking operations turned profitable for the first time in 2025. Two subsidiaries -- UCB Investment Limited and UCB Stock Brokerage Limited -- received Euromoney Awards for Excellence this year, with UCB Investment named Best Investment Bank in Bangladesh 2025.

The operating environment remains difficult. Private investment has been subdued, and growth projections are modest. But Zahir sees room for disciplined expansion.

“UCB currently supports approximately 8 percent of Bangladesh’s international trade,” Zahir says, adding that the bank’s longer-term plan is to rebalance its portfolio by reducing concentration in large corporate exposures while expanding retail and SME lending. It also plans to reach underserved segments through digital channels.

The rebuild will take time. But a shift in approach has come. “Ethical banking is not only about avoiding wrongdoing,” the UCB chair says. “It is about serving customers transparently, responsibly, and consistently. That is the UCB we are building.”

“Once you become a customer of UCB, we will take care of you,” Zahir says. “If you have a genuine business, integrity, and long-term commitment, we will stand beside you.”

Comments