Life insurers face mounting unpaid claims, now at 12 lakh

Monjur Rahman took out a policy with Fareast Islami Life Insurance Company in 2012 to secure his financial future. When it matured in 2022 with a claim of Tk 11.19 lakh, he submitted all the required documents but has yet to receive any payment.

“When I contacted the company, I faced repeated delays and obstacles. Even when my father was hospitalised, I requested a partial payment to cover medical expenses, but I still did not receive any money,” Rahman said.

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. Under the Insurance Act 2010, insurers are required to settle claims within 90 days of receiving all necessary documents.

Payments to life insurance policyholders continue to face heavy delays as the sector grapples with a deepening liquidity crisis. In 2023, around 10 lakh policyholders were waiting for payouts from 29 companies, with Tk 3,050 crore in unpaid claims.

The situation has since deteriorated.

According to the latest data from the Insurance Development and Regulatory Authority (Idra), about 12 lakh policyholders remain unpaid, with 32 insurance companies struggling to clear dues and seven showing the lowest settlement rates. Unsettled claims have grown to Tk 4,403 crore till 2025.

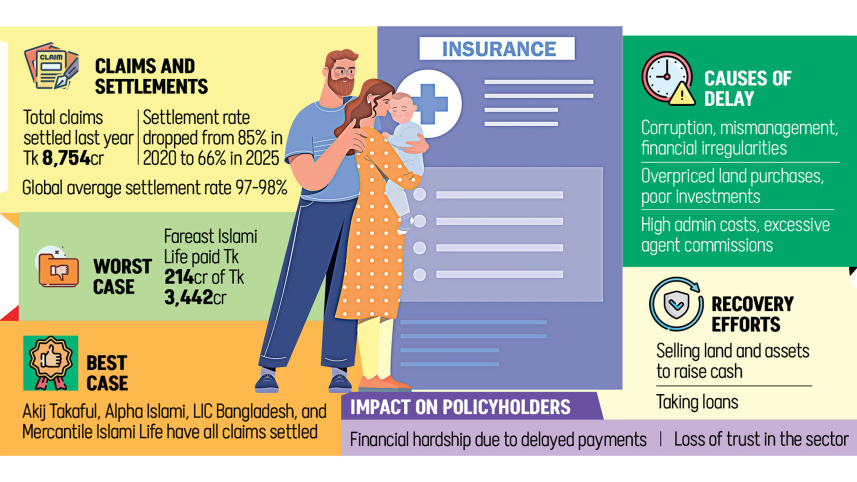

Officials and experts attribute the crisis to financial irregularities, mismanagement, corruption, poor investments, high costs, and unhealthy competition. Companies are now seeking asset sales, loans, and recovery plans to resume payments, all while facing financial strain and weak regulatory oversight.

In the past year, life insurers settled Tk 8,754 crore in claims, covering 66.06 percent of the total claims filed. Claim settlement rates among life insurers have dropped from 85 percent in 2020 to 66.06 percent in 2025, Idra’s data shows.

By comparison, the global average is around 97-98 percent, and in neighbouring India, it was about 98 percent in the 2022-23 fiscal year, according to media reports.

SETTLEMENT RATES AS LOW AS 1.6%

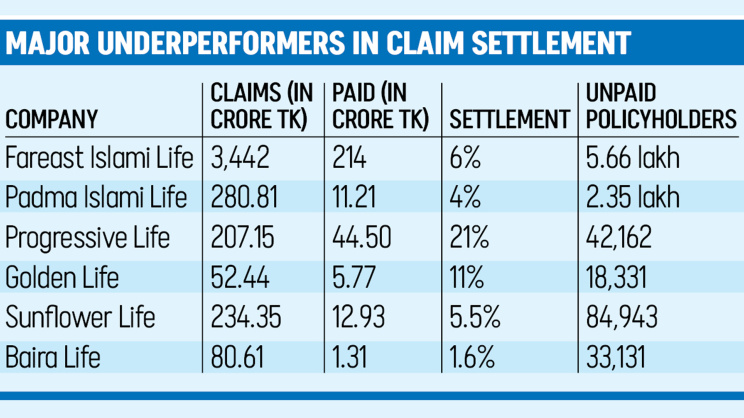

Fareast Islami Life Insurance reported claims of Tk 3,442 crore but paid only Tk 214 crore, leaving 5.66 lakh policyholders still waiting for Tk 3,228 crore.

Its settlement rate was just 6 percent.

An audit commissioned by Idra in 2021 found Tk 2,367 crore had been embezzled, alongside accounting irregularities worth Tk 432 crore at the company.

The report said much of the money had been siphoned off through inflated land purchases and by taking bank loans secured against the company’s Mudaraba Term Deposit Receipts (MTDRs).

An MTDR is a profit-bearing account under the Mudaraba system, which pays returns on deposits held for a fixed period.

Several other life insurers also performed poorly.

Padma Islami Life Insurance settled only 4 percent of its obligations, while Progressive Life Insurance paid about 21 percent.

Golden Life Insurance managed 11 percent, and Sunflower Life Insurance just 5.5 percent. Baira Life Insurance paid only 1.6 percent of claims.

By contrast, Akij Takaful Life Insurance, Alpha Islami Life Insurance, Life Insurance Corporation of Bangladesh, and Mercantile Islami Life Insurance have settled all their claims.

INSURERS CITE PAST MISMANAGEMENT

Abdur Rahim Bhuiyan, chief executive officer (CEO) of Fareast Islami Life Insurance Company, said the company’s backlog of claims is caused by past financial irregularities, corruption, and fund misappropriation, which caused a severe liquidity crisis.

“The board plans to sell some land assets by 2026 and may take loans to improve cash flow,” he added.

Bhuiyan also said the company aims to make significant claim payments this year.

Noor Mohammed Bhuiyan, CEO of Baira Life Insurance Company, said the firm has faced challenges since 2010, including management changes and an Idra-appointed administrator.

He added that land and building investments by previous management are now worth much less.

“We have Idra approval to sell assets, including a Malibagh property acquired for a metro rail station,” Bhuiyan said.

Amzad Hossain Khan Chowdhury, CEO of Golden Life Insurance, said pending claims and limited funds have made operations difficult.

“We requested government loans through the Bangladesh Insurance Association two months ago. Tk 20-Tk 25 crore could help smaller companies recover, but we have received no update,” he added.

Chowdhury highlighted past irregularities between 2011 and 2014, such as unreported policies and missing money receipts, which created claim backlogs. “When clients claimed their funds, the money remained pending,” he said.

He added that after the political changeover in August 2024, operational funding stopped, halting many claim settlements.

Morshed Alam Siddiqui, managing director of Padma Islami Life Insurance, said the company faces a liquidity crisis, which is slowing claim settlement.

He acknowledged that past mismanagement and fund misappropriation contributed to the problem.

“We are trying to sell plots of land to improve cash flow, but buyers offer less than the purchase prices. Previous attempts before the national election failed,” he said.

Saidul Amin, CEO of Progressive Life Insurance, said that mismanagement from 2020 to 2023, along with irregularities in land purchases between 2010 and 2015, contributed to the liquidity crisis and delayed claim settlements. Bad investments worth around Tk 30 crore worsened the situation.

“The Bangladesh Securities and Exchange Commission reconstituted our board in July 2023, and we are now following a three-year recovery plan,” Amin added.

Adeeba Rahman, first vice-president of the Bangladesh Insurance Association and sponsor director of Delta Life Insurance, said the decline in claim settlements is due to institutional mismanagement and severe financial stress.

“Many companies operate with almost depleted funds. Premium income is often diverted to excessive administrative costs or investments benefiting personal interests, causing serious liquidity shortages,” she added.

Rahman added that there have been allegations against some chairmen and directors for embezzling hundreds of crores. Political changeover in 2024 and economic uncertainty weakened public confidence, and the situation worsened in 2025.

She also criticised the regulator for failing to enforce the 90-day claim settlement rule. “Declining investment is largely due to fund shortages and growing mistrust in the sector,” she said.

WEAK OVERSIGHT LEAVES CUSTOMERS WAITING

Md Main Uddin, professor of Banking and Insurance at the University of Dhaka, said poor performance in 2024 carried over into 2025 due to earlier disruptions.

“Many companies failed to earn enough on investments, limiting their ability to pay claims. In some cases, claims were deliberately not paid.”

Uddin added that older insurers are trapped in unprofitability and long claim backlogs. “Some avoid settlements because they expect little legal consequence.”

He said that without regulatory reforms, such as consolidating weak companies and expanding mandatory health insurance, the sector will struggle to match the country’s economic growth.

Md Apel Mahmud, a lifetime member of Idra, said the drop in settlement rates is caused by major discrepancies in company practices. “Some companies report large claim amounts but pay only a small portion,” he said.

He added that mismanagement worsened by possible embezzlement contributes to the problem, although exact amounts are unconfirmed.

Mahmud noted that some company boards lack the will to resolve claims promptly.

He also highlighted regulatory limits, saying, “Idra can suspend boards or cancel registrations, but such actions often trigger public unrest, with customers blaming the authority.”

Comments