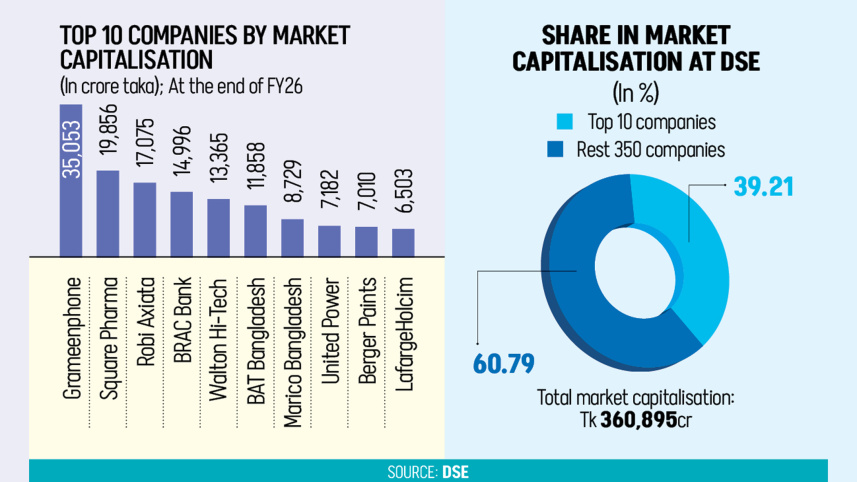

Only 10 firms make up 40% of DSE market value

Although 360 companies are listed on the Dhaka Stock Exchange (DSE), just 10 account for nearly 40 percent of its total market capitalisation, showing the limited depth of the local capital market.

Analysts say the concentration leaves investors with relatively few quality stocks, discourages institutional participation and keeps the market small compared with regional peers.

Grameenphone, the country’s largest listed company, alone accounts for almost one-tenth of the DSE’s total market capitalisation of Tk 360,895 crore. It is followed by Square Pharmaceuticals and Robi Axiata. Together, the three companies make up about one-fifth of the market value.

Market capitalisation is calculated by multiplying a company’s share price by its outstanding shares. The combined value of all listed companies represents the total market capitalisation of the exchange.

Majority-owned by Norway’s Telenor, Grameenphone ended fiscal year 2025-26 with a market value of Tk 35,053 crore. It had 135 crore outstanding shares, while its stock closed the year at Tk 259.

According to DSE data, Square Pharmaceuticals ranks second with a market capitalisation of Tk 19,856 crore, followed by Robi Axiata at Tk 17,075 crore. BRAC Bank, Walton Hi-Tech Industries, British American Tobacco Bangladesh, Marico Bangladesh, United Power Generation, Berger Paints and LafargeHolcim Bangladesh complete the top 10.

“This shows that the market has a lower number of giant companies,” said Saiful Islam, president of the DSE Brokers Association (DBA). “When the market does not have enough good and big companies, investors do not feel interested in coming here.”

Weak investor participation is reflected in the sharp fall in beneficiary owner (BO) accounts, which dropped to 16.75 lakh at the end of fiscal year 2025-26 from 31.53 lakh on July 1, 2016.

Saiful said the market needed more large, fundamentally strong companies and suggested direct listing could be considered to bring some of them onto the exchange.

The shrinking pool of highly valued companies has become more visible after the removal of the floor price mechanism.

Beximco, which had a market value of Tk 10,385 crore only a few months ago while its share price remained fixed under the floor price, has since seen its valuation fall to Tk 2,763 crore as the stock declined sharply.

After the political changeover in August 2024, the company faced a series of setbacks. Its factories remained closed, it has not published financial statements for the past two years, and its share price dropped to Tk 28 on Thursday last week from Tk 110 two months earlier.

FEW HIGH-VALUE COMPANIES

Shahidul Islam, chief executive officer of VIPB Asset Management, said Bangladesh simply has too few companies capable of achieving large market valuations.

“There are a few large business groups, but the number of truly large companies is limited,” he said.

According to him, multinational firms such as Standard Chartered, HSBC and MetLife could each have exceeded Tk 10,000 crore in market value had they operated as locally listed companies instead of branches. Unilever and several local banks also have similar potential.

Bangladesh has only five listed companies with market capitalisation exceeding $1 billion. Grameenphone is valued at $2.84 billion, followed by Square Pharmaceuticals at $1.61 billion, Robi Axiata at $1.38 billion, BRAC Bank at $1.23 billion and Walton Hi-Tech Industries at $1.08 billion.

By comparison, Pakistan’s largest listed company Oil & Gas Development Company has a market capitalisation of $5.17 billion. Six Pakistani companies are valued above $2 billion and nine exceed $1 billion.

Shahidul said many Bangladeshi businesses have failed to build sustainable, profit-driven enterprises. “One of the main reasons is that many businesses in Bangladesh are not run primarily to generate sustainable profits but rather to facilitate rent-seeking and asset extraction.”

“The banking sector, for example, should have produced several banks with valuations of this scale. Instead, widespread looting and capital flight have prevented them from reaching that level.”

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. “A company valuation is fundamentally based on its future profit potential. Therefore, if a company cannot generate strong and sustainable earnings, it will never achieve a high valuation,” he said.

He said highly valued companies usually shared several characteristics, including strong business fundamentals, genuine profitability, sound corporate governance, quality products and services, and a consistent ability to create value for shareholders.

“Unfortunately, many companies in Bangladesh lack this fundamental business mindset and good intentions. As a result, they fail to command high valuations.”

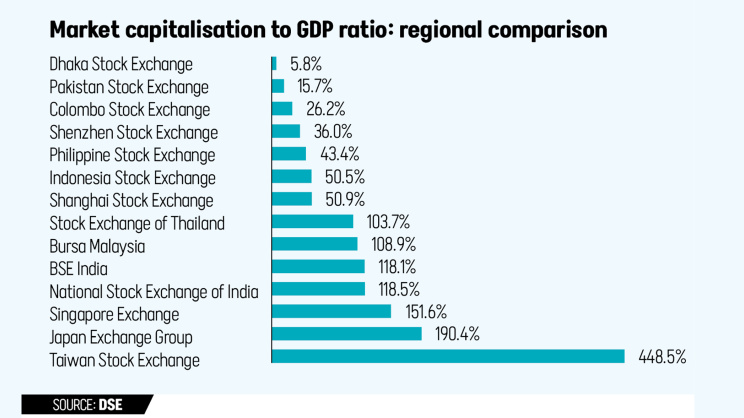

He also said many companies underreported profits to reduce tax liabilities, contributing both to Bangladesh’s exceptionally low tax-to-GDP ratio and its low market capitalisation-to-GDP ratio.

LARGE FIRMS REMAIN OFF THE MARKET

Prof Abu Ahmed, chairman of the Investment Corporation of Bangladesh (ICB), said Bangladesh’s largest companies remain much smaller than those in comparable economies.

“Leaving aside international comparisons, the gap is massive even when compared to our neighbours. For instance, compared to any of the top ten companies in India, our large companies are only a quarter of their size.”

“Even the pharmaceutical companies in Sri Lanka or Pakistan are much larger than ours,” he added. “Among the companies in our country, only Grameenphone might come close in size to similar telecom companies in Pakistan or Sri Lanka.”

Prof Ahmed said it is natural for the top 10 companies to account for around 40 percent of market capitalisation. However, the broader problem is the shortage of large listed companies.

“It is quite natural, nothing unusual at all, for the top ten companies in our market to contribute 40 percent of the total market share. In fact, this is a good thing in one aspect; at least these large companies adhere to rules and regulations and regularly pay out dividends, which works in favour of general investors.”

He said Bangladesh has several large and successful businesses that have chosen to remain outside the stock market.

He cited Unilever and Incepta as examples.

“A multinational company like Unilever is two to three times larger than others, and a pharmaceutical company like Incepta ranks second in terms of turnover, yet they are not on the stock exchange. It is vital for these kinds of good, large companies to enter the capital market.”

“One of the major limitations of our economy is that, to this day, not a single company from Bangladesh has become globally known. To change this scenario, our promising companies must not only maintain high quality but also grow significantly in size,” Ahmed concluded.

Comments