Regular earnings calls could boost foreign investor confidence

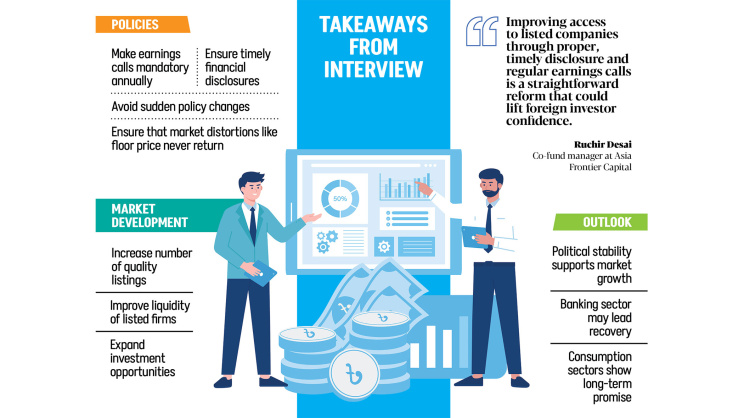

The government should require listed companies to hold at least one annual earnings call and publish financial reports on time to improve transparency and attract foreign investors, said Ruchir Desai, co-fund manager at Asia Frontier Capital, in an interview with The Daily Star.

An earnings call is a conference in which a public company management team speaks with analysts, investors and the media to review results and discuss prospects.

Desai co-manages the AFC Asia Frontier Fund and has been with Asia Frontier Capital since its founding in June 2013. He manages $27 million in assets.

His largest frontier market exposure is in Pakistan, followed by Sri Lanka. Bangladesh ranks fourth among these investment destinations, accounting for about 12 percent of total assets.

Desai said improving access to listed companies through proper, timely disclosure and regular earnings calls is a straightforward reform that could lift foreign investor confidence.

Alongside better disclosure, he called for more quality listings and fewer abrupt policy shifts.

The foreign fund manager said sudden regulatory changes and market interventions that distort price discovery, such as the floor price, should be avoided to maintain confidence.

Desai added that Bangladesh has around 300 listed companies, many of them small and of limited interest to foreign or institutional investors.

According to him, some companies are reasonably liquid, others are not. Even well-run businesses often suffer from thin trading, making it difficult for investors to build meaningful positions.

“I have around 30 shortlisted companies. Of them, I have investments in nine companies.”

In Pakistan and Vietnam, his shortlist is more than double the size of that in Bangladesh. Opportunities are limited here, he said. It should be expanded by bringing more strong companies to market and improving liquidity in existing stocks.

Desai pointed out that access to company management is another constraint. Some profitable firms do not hold even a single earnings call in a year.

“Every company should have an earnings call at least once a year and make it mandatory so that foreign investors can meet the companies and have an idea what’s going on in the companies.”

In Pakistan, at least one annual earnings call is mandatory, he said.

“I know they have an annual report, but when you meet a company face to face, you know you get a better idea of what’s going on.”

He added that regular engagement can also improve valuations and market capitalisation, supporting broader market development.

Timeliness is another issue. In Bangladesh, some companies take four, five or even six months to publish annual financial statements.

Under international best practice, Desai said, annual reports should be released within two months of the year-end.

On past policy measures such as the interest rate cap in banking and the floor price in the stock market, he said, “This kind of mismanagement hit investor confidence hard and exposed the market’s biggest weakness.”

During the roughly two years when the floor price was in place, he said he was unable to execute any trades. “That’s why you don’t see any foreigners in the market now.”

For all latest news, follow The Daily Star's Google News channel.

For all latest news, follow The Daily Star's Google News channel. He said foreign investors will avoid markets where sudden regulatory changes can undermine funds. By preventing share prices from falling below a set level, the floor price created artificial pricing and “zero confidence in the transparency” among foreign investors.

He hoped that it would not be reinstated.

Despite these concerns, Desai expressed optimism. The removal of the floor price was a significant relief and an important step towards attracting investors.

He pointed to improving macroeconomic conditions and renewed political stability. The current account has stabilised, inflation remains high but is easing, and the exchange rate is steady. A national election held two months ago has produced a new government with a clear majority.

A credible election, he said, can act as a catalyst for a market rally by restoring confidence. “The platform is now in place. The authorities must follow through with consistent policymaking and implementation to draw investors back, both foreign and domestic.”

Desai said one priority is listing larger companies to deepen the market. That would boost confidence and, crucially, improve liquidity.

He said investor participation in Bangladesh is low and is declining. To attract retail investors, the market needs stronger companies and more diverse products. The mutual fund industry remains small and requires development.

In India, he added, mutual funds have expanded rapidly over the past 15 years as households increasingly view them as long-term investments rather than short-term trading vehicles.

According to Desai, political stability and low valuations have created room for stronger growth than in the past two or three years.

In the short term, he said the banking sector could lead any rally once external risks such as the war in the Middle East ease.

Private sector credit growth in Bangladesh stands at about 6 percent, which he said is extremely low. “If GDP growth recovers to 5 or 6 percent or higher, banks usually lead because they are leveraged to the wider economy. Some well-run banks are still trading at big discounts.”

He also favours consumer-focused stocks, citing the country’s favourable demographics. These include healthcare and pharmaceutical companies, consumer appliance makers and fast-moving consumer goods producers.

Comments